Most guides treat this as a simple comparison. It isn't. The two paths differ in capital requirements, risk exposure, income mechanics, and the day-to-day reality of ownership. A residential investor who jumps into commercial before they're ready can find themselves underwater fast. A commercial investor who underestimates residential complexity faces similar problems.

This guide covers definitions, a side-by-side comparison, key financial differences — financing, returns, taxes — and a practical framework for deciding which path fits your situation.

TL;DR

- Commercial real estate covers business properties — offices, retail, warehouses, industrial, and 5+ unit multifamily

- Residential real estate covers housing with up to 4 units

- Commercial offers higher income potential but demands more capital, expertise, and tolerance for economic swings

- Residential offers lower barriers to entry, simpler financing, and more stable demand — the natural starting point for most investors

- Commercial loans require 25–35% down, shorter terms with balloon payments, and NOI-based underwriting — residential financing is easier to qualify for

- Most investors start residential, build equity and experience, then transition to commercial

Commercial vs. Residential Real Estate: Quick Comparison

| Factor | Commercial | Residential |

|---|---|---|

| Typical down payment | 15–35% (conventional); 10–15% (SBA 504) | 15–25% (conventional investment); 3.5% (FHA, owner-occupied) |

| Expected cash-on-cash return | 6–12%+ (varies widely by type) | 6–10% (per industry benchmarks) |

| Typical lease length | 3–10 years depending on property type | Month-to-month to 1-year standard |

| Management complexity | High — complex leases, zoning, tenant negotiations | Moderate — higher turnover, maintenance-intensive |

| Risk profile | Higher cyclical exposure; vacancy harder to absorb | More stable demand; recession-resistant |

Note on the 5-unit rule: The dividing line between residential and commercial classification is 5 units. Fannie Mae's Selling Guide purchases mortgages for 1–4 unit residential properties only; 5+ units fall under commercial lending frameworks. Multifamily properties can qualify under either framework depending on unit count — a fourplex uses residential financing, a 6-unit building does not.

What Is Commercial Real Estate Investing?

Commercial real estate is any property used to generate business income or leased to business tenants. The five core property types:

- Office — from single-tenant suburban buildings to Class A urban towers

- Retail — strip malls, standalone stores, shopping centers

- Industrial/warehouse — distribution centers, flex spaces, manufacturing facilities

- Multifamily (5+ units) — apartment complexes, large residential communities

- Hospitality — hotels, motels, short-term accommodation facilities

Industrial and warehouse spaces have seen particularly strong demand in recent years. JLL's Q1 2026 U.S. Industrial Market report recorded net absorption of 50.9 million square feet — an exceptionally strong quarter — with leasing activity up 17.8% year-over-year. E-commerce is the primary driver, pushing consistent need for last-mile logistics and distribution facilities.

How Commercial Properties Generate Income

Commercial income differs from residential in two structural ways that matter to investors.

First, lease structures shift costs to tenants. Under a triple net (NNN) lease, the tenant pays property taxes, insurance, and maintenance on top of rent — the landlord collects a cleaner income stream with fewer surprise expenses.

Second, commercial properties are valued based on income, not comparables. The formula: NOI ÷ Cap Rate = Property Value. This means if you increase rent, you directly increase the appraised value of the property. A residential landlord who raises rent by $200/month pockets extra cash flow. A commercial landlord who raises NOI by $20,000/year may add $300,000+ to property value, depending on the cap rate in that market.

Who Commercial Investing Is Suited For

- Investors with substantial capital and prior real estate experience

- Business owners who want to own their operating space instead of paying rent indefinitely

- Investors comfortable with complex lease negotiations and longer hold periods

Industrial and Warehouse: A More Accessible Entry Point

For investors who want commercial exposure without the complexity of office or retail, industrial and warehouse units offer a practical entry point. NavPoint Real Estate identifies small-bay industrial — multi-tenant units of 1,000–10,000 sq ft priced under $5M — as the most accessible commercial real estate entry point for individual investors, with SBA financing available for owner-occupants and a tenant base that skews recession-resilient.

Personal Warehouse operates squarely in this category — offering purchasable warehouse units across Montana, Colorado, Texas, Florida, and other markets. Financing through SBA 504 and 7(a) programs is available, with terms structured to be as accessible as a residential loan. That combination makes ownership realistic for small business owners, collectors, and operators who'd rather build equity than write rent checks indefinitely.

For those not ready for direct ownership, REITs and commercial real estate funds offer passive exposure — though without the equity-building and customization that come with owning the unit outright.

What Is Residential Real Estate Investing?

Residential real estate covers properties used for housing: single-family homes, condominiums, duplexes, triplexes, and apartment buildings with four or fewer units. That 4-unit cap is the hard boundary for residential lending — cross it and you're in commercial financing territory.

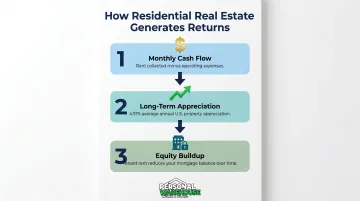

How Residential Properties Generate Returns

Three mechanisms work together:

- Monthly rental cash flow — rent collected minus mortgage, taxes, insurance, and maintenance

- Long-term appreciation — U.S. house prices have averaged 4.51% annual appreciation from 1992 through 2026, with significant variation by market and cycle

- Equity buildup — each mortgage payment made with tenant rent reduces the loan balance

Key Advantages of Residential Investing

- Lower capital requirements than commercial

- Simpler financing backed by personal income and credit score

- Broader tenant pool — people always need housing

- More stable demand during downturns (rental vacancy actually fell during COVID-19, dropping to 5.8% in Q1 2022 — below any point in the prior 35 years)

- Easier resale liquidity compared to commercial properties

Common Residential Strategies

- Buy-and-hold rentals — acquire, rent, hold for appreciation and cash flow

- House hacking — live in one unit of a duplex or triplex while tenants cover most of the mortgage

- Fix-and-flip — renovate and sell for profit; lucrative in rising markets, high-risk during downturns

Residential investing is a natural starting point for:

- First-time investors working with limited capital

- Those who qualify for loans on personal income and credit

- Investors who want direct, hands-on management experience

That accessibility is also its ceiling. Once you need larger returns, portfolio diversification, or longer lease stability, commercial properties enter the picture.

Returns, Risks, and Financing: A Side-by-Side Look

Return Potential

Both asset classes can generate attractive cash-on-cash returns in the 6–12% range, but the mechanism differs:

- Residential returns follow comparable market sales — your property is worth what similar nearby homes sell for, largely outside your control

- Commercial returns are driven by NOI — operational improvements that increase income directly increase property value, giving investors more control over value creation

Risk Profiles

Commercial risks:

- Higher exposure to economic cycles — office vacancy climbed to 18.6% in Q1 2026, a structural shift driven by remote work

- Longer vacancy periods are harder to absorb, especially with balloon payment debt coming due

- Single anchor tenant loss can be financially devastating

Residential risks:

- Higher tenant turnover and maintenance demands

- Tenant protection laws can complicate and delay evictions

- But demand stays relatively stable — housing is a necessity even in recessions

Not all commercial property carries equal risk. Industrial/warehouse fundamentals remain strong, driven by sustained e-commerce demand. Office space faces long-term structural decline from remote work. The real decision isn't commercial vs. residential — it's which property type fits your risk tolerance and market thesis.

Financing Mechanics

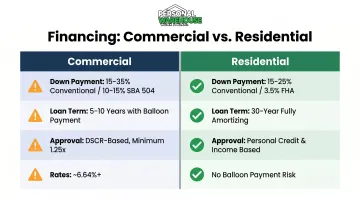

Commercial loans:

- Down payments: 15–35% conventional; 10–15% via SBA 504

- Loan terms: 5–10 years, amortized over 20–30 years, with balloon payments at maturity — creating refinancing risk

- Approval based on property's Debt Service Coverage Ratio (DSCR), typically minimum 1.25x

- Higher interest rates than residential (industrial building loans starting around 6.64% as of mid-2026)

Residential financing works differently — terms are longer, approval criteria are personal rather than property-based, and there's no balloon payment exposure.

Residential loans:

- Conventional investment loans: 15% down (single unit), 25% down (2–4 units)

- FHA loans for owner-occupied: as low as 3.5% down

- 30-year fully amortizing terms — no balloon payment risk

- Approval based on personal credit and income, not property metrics

Tax Considerations

| Factor | Residential | Commercial |

|---|---|---|

| Depreciation schedule | 27.5 years (larger annual deductions) | 39 years (smaller annual deductions) |

| Capital gains exclusion on sale | Up to $250K/$500K on primary residence | Not available |

| 1031 exchange eligibility | Yes (investment properties) | Yes |

The IRS depreciation advantage clearly favors residential investors. The Section 121 exclusion — up to $500,000 tax-free gain for married couples on a primary residence sale — is unavailable for commercial properties. That said, both asset classes qualify for 1031 exchanges — a powerful tool for rolling gains into the next deal without an immediate tax hit. Consult a CPA before assuming either structure optimizes your specific situation.

Which Investment Path Is Right for You?

Start with Residential If You:

- Have limited capital and need residential loan terms to get started

- Are newer to real estate and want a manageable learning curve

- Prefer qualifying for loans based on personal income and credit

- Want hands-on management with direct control over the asset

- Can tolerate higher tenant turnover in exchange for lower barrier to entry

Target Commercial If You:

- Have substantial capital and prior real estate experience

- Want longer lease terms and less frequent tenant interaction

- Are comfortable with complex negotiations and DSCR-based underwriting

- Seek higher income potential and can absorb greater cyclical risk

- Want NOI-driven value creation rather than comparable-sales-driven appreciation

The Proven Progression

Most experienced investors follow a clear path: build experience and equity through residential (1–4 units), generate cash flow, then transition into commercial as capital grows.

For small business owners, collectors, or operators ready to move directly into commercial ownership, Personal Warehouse units offer a practical entry point. Available across markets including Montana, Colorado, Texas, and Florida, units are structured with SBA-eligible financing (504 and 7(a) loans) and ownership terms that reduce the capital threshold typically associated with commercial real estate. Buyers build equity in a commercial asset without needing the resources that traditionally make this asset class inaccessible to individual investors.

Frequently Asked Questions

Is it better to invest in commercial or residential properties?

There's no universal answer. Commercial offers higher income potential and NOI-driven value creation but requires more capital and expertise. Residential provides a lower-risk, more accessible entry point with stable demand. The right choice depends on your financial resources, risk tolerance, and experience level.

What is the 70% rule in flipping?

The 70% rule is a quick guideline for house flippers: never pay more than 70% of a property's after-repair value (ARV) minus estimated repair costs. For example, a home with a $400,000 ARV and $50,000 in repairs means a maximum purchase price of $230,000 , which leaves enough margin for holding costs and profit.

What is the main difference between commercial and residential real estate?

The core distinction is use and unit count. Commercial properties are used for business purposes or contain 5+ rental units; residential properties are for housing with up to 4 units. This classification governs zoning, financing terms, lease structures, and how properties are valued.

What is a triple net lease and why does it matter to investors?

A triple net (NNN) lease requires the tenant to pay property taxes, insurance, and maintenance on top of base rent — shifting most ownership expenses to the tenant. For landlords, this creates a more predictable, lower-effort income stream with fewer day-to-day management demands than a gross lease.

What types of commercial property are good for beginner commercial investors?

Smaller multifamily properties (5–10 units), small-bay industrial/warehouse units, and NNN single-tenant retail are the most accessible entry points. Industrial units under $5M with SBA financing and NNN leases are particularly well-suited: they combine low management complexity with a recession-resilient tenant base.

Can commercial property ever be financed like a residential property?

Traditional commercial loans differ significantly from residential mortgages in down payment requirements and loan terms. Some owner-occupied commercial properties, particularly warehouse units financed through SBA 504 or 7(a) programs, can qualify for down payments and terms that rival residential mortgages — making commercial ownership a realistic option for first-time buyers.