Introduction

Recessions don't treat all commercial real estate equally. Some asset classes hold occupancy, maintain rents, and keep generating income through downturns. Others collapse fast. Office buildings empty out as remote work persists. Retail centers bleed tenants when consumer spending pulls back. Hotels run at 40% occupancy while carrying debt loads built for better times.

What separates those outcomes comes down to what a property does, who uses it, and whether that demand survives when the economy contracts.

Most investors think about recession resilience after the warning signs appear. By then, refinancing costs have risen, lenders have tightened underwriting standards, and the repositioning windows worth having have already closed. Evaluating your CRE allocation before a downturn — not during one — is what separates defensive portfolios from reactive ones.

This guide breaks down which asset types have historically held up, what makes them durable, and how to stress-test any CRE opportunity before conditions force your hand.

TL;DR

- Recession-resistant CRE assets share four traits: essential-use demand, strong location fundamentals, long-term leases, and low capex requirements

- The most durable asset types in downturns are self-storage, industrial/flex warehouse, medical office, multifamily (Class B), and grocery-anchored retail

- Traditional office and non-essential retail are the highest-risk CRE sectors heading into any downturn

- Owning flex warehouse space converts a recurring rent expense into an appreciating hard asset with multiple exit options

What Makes a CRE Investment Truly Recession-Resistant?

Recession resilience in CRE comes down to one question: is demand tied to things people cannot stop doing? Getting healthcare, storing belongings through a life disruption, buying groceries, finding a place to live — these needs hold regardless of unemployment rates or consumer confidence.

The Excelsior Capital framework identifies four characteristics that recession-resistant CRE assets consistently share:

| Characteristic | What It Means in Practice |

|---|---|

| Strong location fundamentals | Markets with sustained population or employment growth |

| Essential or non-discretionary demand | Tenants in healthcare, storage, logistics, grocery |

| Sufficient cash flow | DSCR high enough to absorb temporary income disruption |

| Modest capital needs | Low ongoing maintenance costs to stay operational |

The asset types below have demonstrated these characteristics through multiple economic cycles. None are immune to downturns, but their demand holds where discretionary assets falter — and that gap widens the deeper a recession runs.

The Most Recession-Resistant CRE Asset Types

Selection here is based on historical performance during downturns, occupancy resilience, demand tied to essential services, and investor return patterns across multiple cycles.

Self-Storage Facilities

Self-storage's recession resilience comes from an uncomfortable reality: when people's lives fall apart, they need somewhere to put their stuff. The "four Ds" — downsizing, divorce, dislocation, and death — are the core demand drivers, and recessions accelerate all four simultaneously.

The data backs this up. Self-storage REITs posted a positive 5% total return in 2008 — the only real estate sector to do so — while most other REIT categories suffered losses. The demand mechanism is structural: economic stress creates the exact life disruptions that generate storage need.

For investors, self-storage offers several practical advantages:

- Low management overhead relative to multifamily or retail

- Flexible lease terms that allow rapid repricing when market conditions shift

- Straightforward tenant exit process compared to commercial leases with legal complexity

- High tenant switching costs — once someone is renting a unit near their home, the friction of moving their belongings elsewhere keeps them in place longer than expected

Key metrics to evaluate before buying: local market vacancy rates, unit mix flexibility (small units vs. large), and whether you're competing against institutional operators with pricing power or independent facilities with weaker capital positions.

Industrial & Flex Warehouse Spaces

Industrial real estate's recession resilience is structural, not cyclical. E-commerce drove 23.2% of retail sales (excluding autos and gasoline) in Q3 2024, and that figure is projected to reach 25% by end of 2025. That volume requires warehouse and distribution space regardless of whether GDP growth is positive or negative.

JLL reports the national industrial vacancy rate at 7.5% in Q1 2026, with shallow-bay industrial — buildings under 50,000 sq. ft. — running even tighter due to persistent demand from last-mile logistics and small business operators.

Flex warehouse is a particularly compelling entry point for smaller investors:

- Versatile use cases (business operations, personal storage, RV/boat storage, fabrication, creative office)

- Long-term lease structures with stable income

- Ownership builds equity — the unit appreciates as a hard asset rather than disappearing as rent payments

Personal Warehouse operates in this space, developing and selling flex warehouse units across markets in Montana, Colorado, Texas, and the Southeast. Their model uses SBA 504 and 7(a) financing through preferred lenders to make ownership accessible to individual buyers who would otherwise face institutional barriers to entry.

When evaluating industrial or flex warehouse assets, prioritize: ceiling height, drive-in access, proximity to population centers, and tenant mix diversity across multiple industries.

Medical Office Buildings (MOBs)

MOBs occupy an unusual position in CRE: the structural demand driver gets stronger every year. By 2030, all Baby Boomers will be at least 65. That's approximately 73 million people, and they currently spend five times more on medical services than younger generations. Healthcare demand doesn't contract in a recession — if anything, deferred care rebounds when conditions improve.

MOB occupancy held at 92.0–93.0% during H1 2025 according to BGL Healthcare Real Estate data, compared to the 18%+ vacancy rates plaguing general office. That gap reflects a fundamental distinction: essential-use properties hold occupancy where discretionary-use properties don't.

Tenant characteristics are equally important:

- MOB tenants sign long-term leases (often 10+ years) with creditworthy hospital systems

- High tenant improvement costs for medical buildouts make relocation extremely unattractive

- Healthcare workers are classified as essential, insulating MOBs from remote-work disruption entirely

For evaluation purposes: anchor tenant credit quality matters most, followed by proximity to hospital campuses or complementary healthcare services, and flexibility for outpatient or specialty care use.

Multifamily & Workforce Housing

During recessions, homeownership becomes less attainable — tighter lending standards, job insecurity, and down payment constraints push households into the rental market. The people most affected are the ones who rent Class B and C workforce housing, and their need for shelter doesn't diminish when the economy contracts.

CBRE research confirms that Class B multifamily outperformed both Class A and Class C assets during past downturns. Class A residents can trade down; Class B residents largely stay put. Market-rate apartment occupancy sat at 95.7% in Q2 2025 per RealPage data, with the demographic pipeline still growing — 72 million Millennials and an estimated 4.3 million additional apartment units needed by 2035.

Secondary markets across the Mountain West, Southeast, and Sun Belt benefit from migration trends and relative affordability compared to coastal gateway cities, which adds another layer of demand durability.

Necessity-Based Retail (Grocery-Anchored Centers)

The key distinction isn't between retail and non-retail — it's between what people buy regardless of the economy and what they cut when budgets tighten. Groceries and prescriptions don't get deferred. Designer clothing and department store discretionary goods do.

During the 2007–2009 recession, grocery-anchored centers maintained occupancy above 90% while general retail saw widespread vacancies. CBRE's H2 2025 Cap Rate Survey ranked grocery-anchored centers first among all retail subtypes for expected investment performance, and U.S. consumers spent over $915 billion on groceries in 2025 — up 21% since 2020.

Resilience indicators to evaluate: anchor tenant type (grocery vs. fashion), location density, lease term length, and the percentage of co-tenants serving essential vs. discretionary needs.

Which CRE Asset Types Struggle in Recessions?

Two sectors carry the most risk heading into any downturn.

Traditional Office has become the most structurally vulnerable major CRE sector. Remote and hybrid work permanently reduced demand — in-office utilization averaged only 48% of pre-pandemic levels across 10 major cities as of April 2024. CBRE recorded overall U.S. office vacancy at 18.6% in Q1 2026, while JLL measured total vacancy at 22.64% in Q1 2025. A recession compounds this by causing companies to reduce footprints or freeze expansion decisions. Office delinquency rates surged from 2.4% in February 2023 to 6.6% in February 2024 — a sign of serious underlying stress.

Office isn't alone in its vulnerability. Non-Essential Retail and Hospitality share the same exposure to cyclical downturns, just through different mechanisms:

- Hotels: RevPAR dropped 20.4% in May 2009 during the Great Recession, with net operating income falling 36.6% year-over-year.

- Department stores and fashion retail: Discretionary spending contracts sharply in downturns, and the tenants who drive foot traffic often don't survive long enough for recovery.

How to Evaluate a CRE Investment for Recession Resilience

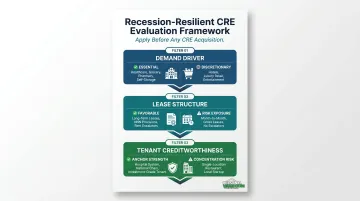

Three Primary Filters

Experienced investors apply these screens before going further on any CRE acquisition:

- Is the demand driver essential or discretionary? Self-storage, healthcare, grocery, housing — essential. Hotels, office, luxury retail — discretionary.

- What is the lease structure? Long terms, NNN provisions, and built-in rent escalators provide income predictability. Month-to-month or short-term leases leave you exposed to occupancy drops at the worst possible time.

- What is the tenant's creditworthiness? A healthcare system anchor in an MOB is fundamentally different credit risk than a single-location restaurant in a retail strip. Default probability during a slow economy should be central to any underwriting.

Location Still Determines Outcomes

A recession-resistant asset type in a weak market is still a risky investment. Four location factors determine how much that resilience actually holds up in practice:

- Population growth trends in the target market

- Job market diversification (single-industry towns carry more risk)

- Supply pipeline constraints limiting new competition

- Proximity to demand centers driving consistent occupancy

Markets with constrained supply pipelines and diversified employment bases — many Sun Belt metros, growing secondary markets in the Mountain West and Southeast — tend to recover faster and see less severe occupancy drops during downturns.

Financing and Liquidity

The OCC recommends a minimum stabilized DSCR of 1.20 for income property lending, with stress testing against a 10% NOI reduction or interest rate increase. Individual investors should target 1.25 or higher entering a potential downturn.

Fixed-rate financing matters as much as DSCR. Approximately $875 billion in CRE loans are scheduled to mature in 2026 — borrowers with floating-rate debt or balloon payments due during a contraction face severe refinancing risk. Cash reserves covering two to three months of vacancies provide the margin needed to hold assets through disruption rather than selling at the bottom.

Conclusion

Recession-resistant CRE investing comes down to a straightforward principle: own assets tied to things people can't stop needing, backed by solid lease structures and creditworthy tenants, in markets with durable demand fundamentals. Self-storage, industrial and flex warehouse, medical office, Class B multifamily, and grocery-anchored retail have earned their defensive reputation through data, not marketing.

For investors exploring direct ownership in the industrial and flex warehouse category, Personal Warehouse offers an accessible entry point across multiple U.S. markets. Their model is structured for individual buyers rather than institutional capital, with:

- SBA-compatible financing carrying residential-style loan terms

- 99-year ground leases for long-term stability

- Customizable units built to hold resale value

The Bozeman, MT project is currently under construction and accepting reservations for 2026 delivery.

Evaluate both the asset type and your ownership structure carefully. In a downturn, those two choices — what you own and how you own it — matter more than market timing.

Frequently Asked Questions

What is the safest investment during a recession?

No investment is entirely risk-free in a recession, but assets tied to essential demand — self-storage, multifamily housing, medical facilities, and industrial real estate — have historically been the most stable. Their demand persists regardless of economic conditions because tenants cannot easily defer or eliminate their space needs.

How do you invest in real estate during a recession?

Focus on essential-use property types, secure fixed-rate financing before rates shift, and maintain liquidity reserves to weather temporary vacancies. Depending on budget and risk tolerance, options include direct ownership of flex warehouse or multifamily units, or indirect exposure through REITs and crowdfunding platforms.

What is the 2% rule in commercial real estate?

The 2% rule is a rough screening tool where a property's monthly rent should equal at least 2% of its purchase price to indicate positive cash flow potential. In CRE, investors more commonly rely on cap rate, DSCR, and NOI — the 2% rule is primarily applied in residential contexts and is too blunt for commercial underwriting.

Is self-storage a good investment during a recession?

Self-storage is one of the strongest-performing CRE sectors during recessions. The "four Ds" — downsizing, divorce, dislocation, and death — drive demand that accelerates during economic contractions. Self-storage REITs were the only real estate sector to post positive returns in 2008, backed by low operating costs and flexible month-to-month leases.

Which commercial real estate sectors should I avoid in a recession?

Traditional office and non-essential retail carry the highest risk. Remote work has structurally reduced office demand, and a recession amplifies that by causing companies to shrink footprints. Department stores and luxury-focused retail centers suffer from sharp consumer spending pullback that directly reduces foot traffic and tenant viability.

Can individual investors own recession-resistant commercial real estate directly?

Direct ownership is accessible well below institutional scale. Options include flex warehouse units, small self-storage facilities, or small multifamily properties. Personal Warehouse offers individual ownership of warehouse and flex spaces with SBA-compatible financing and residential-style loan terms — making this asset class reachable for individual buyers.