The choice between these two asset classes affects more than just yield. It shapes vacancy exposure, lease income predictability, capital requirements, and how much management attention your investment demands year after year.

And the picture looks meaningfully different today than it did 18 months ago — particularly for smaller investors and business owners who want their capital to work hard without requiring institutional-scale resources or expertise.

TL;DR

- Class A office in prime locations is recovering; suburban and Class B/C still face persistent headwinds

- Industrial dipped in Q2 2025 (first negative absorption since 2010), then rebounded sharply — Q1 2026 absorption hit 50.9M SF

- Industrial outperforms office on total return: NCREIF data shows 1.42% quarterly return vs. 0.37% for office

- Small-bay industrial under 100K SF sits at just 4.6% vacancy, the tightest segment in commercial real estate right now

- Owner-operators get a dual advantage with industrial: operational utility plus equity-building that office rarely matches

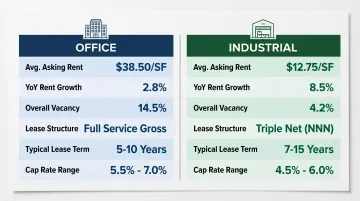

Office vs. Industrial Space: Quick Comparison

Before going deeper on each asset class, here's a side-by-side snapshot of the metrics that matter most to investors in 2026.

| Metric | Office | Industrial |

|---|---|---|

| Avg. asking rent (national) | $37.21/SF (Q1 2026) | $10.10/SF (Q3 2025) |

| YoY rent growth | +2.2% | +1.7% (asking); +6.9% (in-place) |

| Overall vacancy | 18.6% (CBRE Q1 2026) | 7.5% (JLL Q1 2026) |

| Typical lease structure | Gross or modified gross | Triple net (NNN) |

| Typical lease term | 3–7 years | 5–10 years |

| Cap rate range (Class A) | 6.5%–7.5% | ~6.0% |

Office rents run roughly 3.5x higher per square foot — but industrial in-place rent growth at 6.9% annually outpaces office asking rent growth at 2.2% by a wide margin. Industrial tenants currently paying $8.27/SF will eventually roll to new leases at $10.10/SF — that spread is embedded upside waiting to be realized.

Those rent figures only tell part of the story — lease structure determines how much of that income actually reaches you. Industrial NNN leases push property taxes, insurance, and maintenance costs onto tenants, creating cleaner income for landlords. Office gross leases typically leave those expenses with the owner — adding management complexity and eroding net returns.

What Is Office Space as an Investment?

Office investment covers a wide range — Class A urban towers, suburban business parks, and medical office buildings. For investors who are also business operators, office space can offer the appeal of owning your professional environment — though the risk profile has shifted significantly since 2020.

The Flight to Quality

Office demand is consolidating around quality. Tenants are surrendering older, lower-quality space and upgrading into well-amenitized, flexible Class A buildings. The vacancy gap tells the story clearly: Class A office vacancy sat at 14.2% in Q3 2025, versus 19.1% for lower-quality assets — a five-percentage-point spread that's still widening. By Q1 2026, CBRE measured prime vacancy at just 12.7% against an overall market rate of 18.6%.

Return-to-office momentum is providing some floor for demand. Weekly office occupancy reached 54.6% nationally per Kastle Systems, and the share of mostly in-person workers doubled from 34% to 68% between 2023 and 2024.

Sun Belt markets are outperforming the national average by a wide margin:

- Charlotte — deal sizes averaged 141.6% above the five-year average in Q3 2025

- Nashville — seven consecutive quarters of positive absorption

- Dallas Class A — positive net absorption sustained throughout 2025

These are the submarkets where office investment still makes a credible case.

Key Risks to Understand

That said, office investment carries structural headwinds investors need to weigh carefully:

- Tenant improvement costs range from $50 to $150 per square foot, creating significant capital exposure every time a space re-leases

- Longer lease-up timelines mean vacancy can persist for 12–24 months between tenants

- Hybrid work has permanently compressed per-employee square footage needs — companies aren't returning to pre-2020 space ratios

- Capital depreciation compounds the problem — NCREIF data shows office delivering -0.86% appreciation quarterly, meaning landlords collect rent while the underlying asset loses value

Office works best for investors with deep capital reserves, expertise in repositioning, and access to prime urban or mixed-use submarkets. Medical office is the notable exception — structured more like a defensive asset, with portfolio cap rates around 6.5% and 2.8% annual healthcare employment growth providing durable demand.

Office Investment Use Cases

Office investment still makes sense in specific contexts:

- Sun Belt Class A acquisitions in metros like Dallas, Charlotte, Atlanta, or Nashville, where fundamentals are running ahead of the national average

- Medical office buildings, which PwC/ULI classify as "anticyclical" with tight market conditions supporting rent growth

- Sale-leaseback structures where a business owns and occupies its own professional space

- Value-add repositioning of distressed Class A assets purchased at deep discounts — a contrarian play requiring significant expertise and capital patience

What Is Industrial Space as an Investment?

Industrial investment spans a broad spectrum: large-scale distribution centers, flex industrial buildings, manufacturing facilities, and smaller warehouse units. What unifies them is structural simplicity. NNN leases, longer terms, and lower management burden make industrial properties easier to own and operate than almost any other commercial property type.

The 2025–2026 Demand Story

Industrial had a jarring moment in Q2 2025 when net absorption turned negative for the first time since 2010, driven by tariff uncertainty and hesitation around supply chain commitments. But the correction was brief.

Absorption recovered to 45.1M SF in Q3 2025, then hit 50.9M SF in Q1 2026 — what JLL described as "exceptional strength for the period," with leasing activity up 17.8% year-over-year. NAIOP now projects full-year 2026 absorption at 345.9M SF, with H1 2026 alone expected to reach 154.8M SF.

Tailwinds driving this rebound include:

- E-commerce fulfillment — every $1 billion in online sales requires approximately 1.25 million SF of warehouse space

- Automation adoption — new facilities now average 35-foot clear heights to accommodate robotics and vertical storage systems

- Sun Belt population growth — Texas, Georgia, Florida, and the Carolinas are generating outsized regional demand

- Modern spec preference — buildings constructed since 2020 gained 196M SF of net growth in Q3 2025, while older facilities shed 88M SF

The Small-Bay Advantage

The most accessible segment for individual investors and owner-operators is also the tightest. Warehouses under 100,000 SF posted a vacancy rate of just 4.6% in Q3 2025, compared to 7.1% for industrial overall. Less competition, simpler operations, and stronger supply-demand balance make this the clearest entry point for non-institutional buyers.

That dynamic is especially relevant for small business owners weighing a purchase. Owning your operating space means building equity instead of paying a landlord. Personal Warehouse offers customizable, individually-owned warehouse units with SBA 504 and 7(a) financing available through preferred lenders, terms comparable to residential loans, and a 99-year ground lease structure for long-term stability without full land acquisition costs.

Units can be held for personal use, leased to generate NNN-style income, or sold as market conditions evolve.

Industrial Investment Use Cases

Industrial ownership suits a wide range of buyer profiles:

- Trades businesses and contractors needing secure operational storage with equity upside

- E-commerce operators requiring dedicated fulfillment or last-mile distribution space

- Collectors and hobbyists seeking climate-controlled, secure facilities with investment value

- Real estate investors seeking NNN income with low management requirements and long lease terms

- Small business owners who currently rent warehouse space and want to stop paying someone else's mortgage

Office vs. Industrial: Which Is the Better Investment in 2026?

The data doesn't offer a universal answer, but it points clearly enough for most investor profiles to make a confident decision.

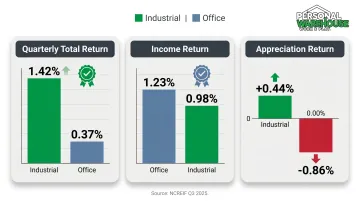

Comparing the Return Profiles

NCREIF's Q3 2025 data provides the starkest head-to-head comparison available:

| Metric | Industrial | Office |

|---|---|---|

| Quarterly total return | 1.42% | 0.37% |

| Income return | 0.98% | 1.23% |

| Appreciation return | +0.44% | -0.86% |

Office actually generates higher income return, but capital depreciation of -0.86% quarterly erodes most of that advantage. Industrial delivers both income and appreciation simultaneously.

For leveraged investors, office's depreciation dynamic is particularly dangerous: you're collecting rent while your collateral loses value.

Timing and Entry Point

Both sectors are in transition in 2026, but in opposite directions.

Industrial cap rates have expanded roughly 150 basis points from their 2021 lows to approximately 6.0% — creating a more attractive entry point than investors have seen in years. The demand rebound is already underway, meaning buyers entering now are positioned ahead of a recovering cycle rather than chasing it.

Office tells a more complicated story. Class A urban assets offer cap rates of 6.5%–7.5%, the highest in years, and CBRE projects office investment volume to rise 20% in 2026. Yet CBRE also ranks office last among all property types for expected 10-year investment performance. Institutional capital has been a net seller of office for eight of the past nine years. Private equity and foreign buyers are selectively acquiring distressed assets at fractions of replacement cost — but selectively is the operative word.

Situational Recommendations

Choose industrial if:

- Cash flow stability and predictability are priorities

- You want lower management burden and NNN lease structures

- Your space needs to serve an operational function while building equity

- You're investing in Sun Belt markets with strong absorption trends

Choose office if:

- You have capital and expertise to reposition underperforming Class A assets

- You're targeting specific high-demand submarkets (Sun Belt Class A, medical office)

- You can tolerate 12–24 month lease-up periods and significant TI exposure

- You're pursuing a contrarian deep-value play at distressed pricing

Real-World Context: How Investors Are Approaching This in 2026

Institutional capital tells an interesting story. REITs have been net sellers of office for eight of the past nine years (Cresa), yet office sales volume rose 21.7% in 2024 — suggesting that private and foreign buyers are stepping into the distressed opportunity. Industrial transactions hit $15.5 billion in Q1 2026 alone, per CommercialCafe citing Yardi Matrix data, pointing to continued transaction activity even as 2021-era pricing compression fades.

That capital is flowing somewhere specific. Sun Belt industrial fundamentals remain among the strongest in the country, with absorption outpacing new supply across several key metros:

- Atlanta: In-place rents climbed 8.1% year-over-year as of early 2026

- Dallas-Fort Worth, Houston, and Phoenix: Each recorded more than 3 million SF of net absorption in Q3 2025

Vacancy pressure stays contained in these markets even as the national average sits near decade highs.

For investors without institutional-scale capital, options do exist in these growth markets. Personal Warehouse offers ownable warehouse units in several of the same high-demand states — including Georgia, Texas, Florida, and the Carolinas — with SBA-eligible financing and a 99-year ground lease structure. It's one way smaller buyers are accessing the industrial sector without waiting for a REIT allocation.

Conclusion

Industrial space enters 2026 with real momentum behind it: recovering absorption, a forecasted demand surge, tight small-bay vacancy, and NNN lease structures that favor passive income over active management. For investors who can also use the space operationally, the dual utility makes the ownership case even stronger.

Office, by contrast, still offers genuine opportunities — but they require selectivity, capital depth, and patience. The gap between Class A Sun Belt assets and everything else is widening, not narrowing. Investors who can identify and acquire the right office assets in the right submarkets may generate strong returns, but the margin for error is narrow and the capital requirements are substantial.

The decision comes down to fit: match the asset's characteristics to your risk tolerance, time horizon, capital position, and operational needs. Industrial rewards patient capital with predictable income. Office rewards conviction and deep pockets with potential upside — provided you pick the right market and the right building.

Frequently Asked Questions

Is there demand for office space?

Yes, but it's sharply bifurcated. Class A space in prime urban markets is seeing strong leasing activity driven by return-to-office mandates and corporate consolidations, while Class B/C and suburban office continues to face elevated vacancy and slow recovery. Location and asset quality determine almost everything.

Is industrial real estate a good investment in 2026?

Industrial is well-positioned for 2026 after a brief demand dip in Q2 2025. With NAIOP projecting 345.9M SF of net absorption for the full year and Q1 2026 already showing 50.9M SF, investors entering now are positioned ahead of an accelerating recovery cycle.

What are the typical returns on office vs. industrial real estate?

Industrial delivers more consistent returns through NNN leases and steady rent growth: NCREIF shows a 1.42% quarterly total return with positive appreciation. Office generates slightly higher income return but carries -0.86% quarterly capital depreciation, which erodes net performance.

Is it better to lease or own industrial space?

Owning builds equity and locks in long-term cost stability, which is particularly valuable for businesses paying rent with nothing to show for it. Leasing offers flexibility but no ownership upside. For operators planning to stay in a market five or more years, ownership typically costs less over time than continued rent payments.

What types of businesses benefit most from owning warehouse space?

Trades businesses, e-commerce operators, contractors, collectors, and any operation requiring secure, functional storage gain the most. Ownership lets these users meet daily operational needs while accumulating equity — something renting cannot offer.

How does remote and hybrid work affect office space investment?

Hybrid work has permanently reduced per-employee square footage requirements, pushing companies to downsize their footprints while upgrading to higher-quality buildings with stronger amenities. This favors Class A assets in prime locations and creates sustained risk for older suburban office stock.