The obstacle isn't motivation. It's clarity. Most buyers don't know which loan type fits their situation, what lenders actually require, or how long the process takes. The wrong loan choice can cost tens of thousands over the life of the deal.

This guide breaks down every major financing path for 2026, from SBA 504 and 7(a) programs to conventional commercial mortgages and alternative lenders. It also covers what lenders evaluate before approving you, how to navigate the application process step by step, and practical ways to improve your approval odds.

One important distinction upfront: "buying a warehouse business" can mean acquiring an operating warehouse business, purchasing a commercial warehouse property outright, or securing an ownership unit in a warehouse development like Personal Warehouse's owner-occupied Micro-Flex condominiums. Each scenario has a different financing path — and this guide covers all of them.

TL;DR

- U.S. industrial net absorption hit 40 million sq ft in Q1 2026, up 52% year-over-year — warehouse demand is recovering fast

- SBA 504 loans allow as little as 10% down for owner-occupied warehouse real estate with fixed rates around 5.95%

- SBA 7(a) loans go up to $5 million and can cover business acquisition, real estate, and working capital in one loan

- Qualify faster by targeting a 680+ personal FICO score and a DSCR of at least 1.20–1.25x before you apply

- Start the financing process 90–120 days before your target closing date

Why Buy a Warehouse Business in 2026?

The market data makes a compelling case. According to Cushman & Wakefield's Q1 2026 Industrial MarketBeat, U.S. industrial vacancy held at 7.0% in Q1 2026 while net absorption surged to 40 million square feet — a 52% jump year-over-year. Supply is also moderating: new completions fell to their lowest quarterly total since mid-2017. For buyers considering a purchase in 2026, that's a rare alignment — demand climbing while new supply dries up.

Owning vs. Renting: The Core Financial Argument

Every rent check you write disappears. Every mortgage payment builds equity. Ownership also delivers practical advantages that renting never can:

- Locks in predictable monthly costs instead of absorbing rent increases

- Gives you full customization rights to configure the space for your operations

- Opens the door to sublease income from unused portions of the property

- Builds long-term appreciation on a tangible asset

Industrial sale prices rose roughly 54% from 2019 to 2022, and while appreciation has cooled since that peak, NAIOP expects absorption to rebound starting Q2 2026 as supply moderates, which positions early 2026 buyers ahead of that demand curve.

A Lower-Barrier Entry Point

The financial case is clear — but it only matters if buyers can actually access the financing. That's where the market has shifted.

Traditional commercial real estate required large down payments and complex underwriting. Personal Warehouse structures its owner-occupied Micro-Flex condominium units around a 99-year ground lease, with financing available through preferred SBA-experienced lenders. The result: terms that compare closely to a residential mortgage, putting ownership within reach for small business owners, collectors, and creative professionals who've historically been priced out of commercial property.

Your Loan Options for Buying a Warehouse Business

No single loan fits every buyer. The right product depends on what you're acquiring, how you'll use it, and your financial profile. Here's how the main options compare.

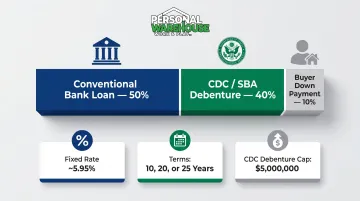

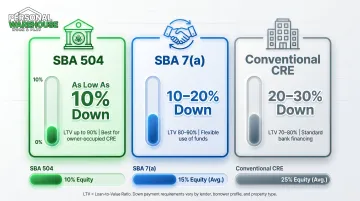

SBA 504 Loans

The SBA 504 program is one of the most cost-effective routes for buying owner-occupied warehouse real estate. Financing splits across three sources:

- ~50% covered by a conventional bank loan

- ~40% covered by a Certified Development Company (CDC) debenture backed by the SBA

- ~10% from the buyer as a down payment

The CDC debenture carries a fixed rate over 10-, 20-, or 25-year terms — currently around 5.95% for a 25-year term as of May 2026. CDC debentures generally go up to $5 million (up to $5.5 million for small manufacturers or qualifying energy projects).

Eligibility basics: for-profit U.S. businesses that meet SBA size standards. The loan must fund fixed assets — purchasing an existing building, new construction, or long-life equipment. It's purpose-built for owner-occupied warehouses.

The SBA also doubled the cumulative 7(a) and 504 loan limit to $10 million in May 2026, expanding access for buyers who need both programs.

SBA 7(a) Loans

The 7(a) program offers more flexibility than the 504. It can fund real estate, business acquisition, equipment, and working capital — all under a single loan up to $5 million with terms up to 25 years for real estate. Key terms at a glance:

- SBA guarantee: 85% on loans ≤$150,000; 75% on larger amounts

- Best use: Buying a warehouse business as a going concern — not just the property

- Advantage: Covers goodwill, equipment, inventory, and real estate under one loan

That guarantee is what opens doors for buyers who don't qualify for conventional commercial financing.

Conventional Commercial Real Estate Loans

Traditional bank commercial mortgages are faster to close than SBA products but require more equity upfront. Typical parameters:

| Feature | Conventional CRE |

|---|---|

| Down payment | 20–30% |

| LTV | 65–80% |

| Loan term | Often up to 10 years (with 20–25 yr amortization) |

| Approval timeline | 30–60 days |

| SBA guarantee | None |

The key advantage is speed and simplicity. The tradeoff: balloon risk at term maturity, stricter documentation, and lender scrutiny of the property's condition, location, and intended use before approval.

Alternative and Private Financing

Hard money lenders, bridge lenders, and online commercial lenders fill gaps when timing is tight, the property is non-standard, or credit falls short of bank minimums. What to know:

- LTV up to ~75% in many cases

- Rates are significantly higher than conventional bank products

- Terms are typically short (12–24 months) — designed for transitional situations, not long-term holds

- Business lines of credit can supplement soft costs or bridge operational gaps during acquisition

Caution: Always evaluate total loan cost, not just the interest rate. Points, origination fees, and default provisions add up quickly on private money deals.

What Lenders Evaluate Before Approving Your Loan

Credit Score and Business Credit

Most SBA and conventional commercial lenders prefer a personal FICO score of 680 or higher. Some alternative lenders work with scores in the 600–650 range, but at worse rates and terms.

Business credit matters too. Dun & Bradstreet's PAYDEX score runs from 1–100, with 80 or above considered low risk by most commercial creditors. Pull both your personal credit report and your D&B report before applying — and resolve any errors before a lender sees them.

Debt-Service Coverage Ratio (DSCR)

DSCR = Net Operating Income ÷ Total Debt Payments

Lenders typically require a minimum of 1.20–1.25x, meaning your income must exceed your debt obligations by 20–25%. A DSCR of 1.0x is break-even; anything below signals repayment risk.

Calculate your estimated DSCR before submitting an application. If you're buying an income-producing warehouse, use the property's actual NOI. For owner-occupied purchases, lenders often consider the business income that would otherwise go toward rent.

Down Payment and LTV

Required down payments vary by loan type:

- SBA 504: as low as 10%

- SBA 7(a): varies by lender; typically 10–20%

- Conventional CRE: 20–30%

A larger down payment does more than reduce your monthly payment — it lowers lender risk, which can mean a better interest rate and faster approval. The 20% benchmark is common but not universal; loan type and lender appetite ultimately set the floor.

Collateral and Personal Guarantees

Warehouse loans are typically secured by the property itself. SBA loans also require personal guarantees from anyone owning 20% or more of the borrowing entity — this is non-negotiable per SBA Form 148.

For specialized or single-use warehouse facilities, lenders may require larger down payments due to lower resale marketability. Standard commercial warehouse spaces are generally easier to collateralize.

Financials, Business History, and Business Plan

SBA and conventional lenders typically require:

- 2+ years of documented business history

- 2–3 years of personal and business tax returns

- Profit and loss statements and current balance sheets

- 3–6 months of bank statements

- Seller's financials (for business acquisitions)

A written business plan carries real weight with underwriters. Lenders want to see how the warehouse will be used, what income or cost savings it generates, and a credible repayment path — weak plans get rejected even when the numbers look acceptable.

How to Apply for a Warehouse Business Loan: Step by Step

Step 1: Define Your Acquisition Type and Budget

Before contacting a single lender, get clear on what you're buying. Is it a warehouse property, an operating business, or a unit in a development? Then build a complete budget:

- Purchase price

- Closing costs (typically 2–5% of loan amount)

- Renovation or fit-out costs (including customizations like HVAC, mezzanines, or restrooms)

- 10–15% contingency buffer

Buyers of Personal Warehouse units, for instance, should factor in available upgrades. Mezzanines can expand usable space by up to 30%, which affects both your budget and the eventual appraised value.

Step 2: Compare Lenders and Get Pre-Qualified

Not all lenders handle warehouse financing the same way. Compare:

- SBA-approved lenders vs. conventional commercial banks vs. alternative lenders

- Minimum credit score requirements

- Loan amounts and approval timelines

- Experience with your specific property type

Seek a pre-qualification letter or term sheet before committing. A commercial mortgage broker can compress this research phase considerably — often cutting weeks off your timeline. Personal Warehouse works with preferred lenders experienced in SBA 504 and 7(a) financing for their owner-occupied units — a useful starting point for buyers considering their projects.

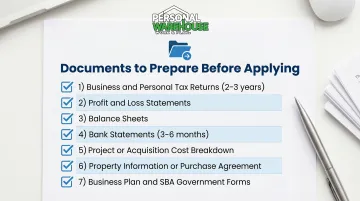

Step 3: Gather Your Documentation

Organize these before submitting any application:

- 2–3 years of business and personal tax returns

- Profit and loss statements and balance sheets

- 3–6 months of bank statements

- Project or acquisition cost breakdown

- Property information or executed purchase agreement

- Business plan

- SBA-required government forms (for SBA loans)

Complete, organized documentation compresses approval timelines more than almost any other factor.

Step 4: Submit, Underwrite, and Close

During underwriting, lenders will:

- Review all financial documentation

- Order a commercial appraisal

- Require a Phase I Environmental Site Assessment (standard for industrial properties per ASTM E1527-21)

- Verify collateral value

Approval timelines by loan type:

| Loan Type | Typical Timeline |

|---|---|

| Alternative/equipment financing | 24–72 hours |

| Conventional CRE | 30–60 days |

| SBA 7(a) or 504 | 60–90 days |

Start the financing process 90–120 days before your target closing date. Order the Phase I ESA early — it's a common bottleneck that delays otherwise clean deals.

Tips to Improve Your Chances of Getting Approved

A few targeted moves before you apply can meaningfully improve your approval odds — and the terms you're offered.

Target a FICO above 680. Pay down revolving debt, dispute any errors on your personal and business credit reports, and give yourself time. Even a 20–30 point improvement can unlock better rates and open doors to programs like SBA 504.

Write a specific business plan. Explain the intended use, projected revenue or operational savings, and a realistic repayment scenario. Lenders approve buyers who understand both the asset and the numbers. For Personal Warehouse unit buyers, documenting the unit's features — LED lighting, high-efficiency insulation, insulated overhead doors — alongside leasing or resale potential strengthens the underwriter's view of collateral quality.

Put more down if you can. Even when low-down-payment programs are available, a larger down payment reduces your monthly obligations, lowers lender risk, and gives you an edge when competing for a unit. Your state's Small Business Development Center (SBDC) or local economic development agency may also offer down payment assistance programs for commercial acquisitions.

Frequently Asked Questions

Do you have to put 20% down on a commercial loan?

No. While 20% is a common requirement for conventional commercial mortgages, SBA 504 loans allow as little as 10% down. The exact requirement depends on loan type, lender policies, and your overall borrower profile.

Can I get a $100,000 SBA loan?

Yes. SBA 7(a) loans can be issued in amounts well under $100,000, and the SBA Microloan program provides up to $50,000 for qualifying small businesses. This range suits buyers financing a smaller warehouse unit or covering acquisition-related costs.

Is buying a warehouse profitable?

It can be, through three channels: eliminating rent costs, property appreciation, and rental income from subleasing unused space. Industrial sale prices rose roughly 54% from 2019 to 2022, and CBRE projects industrial cap rates to compress further as markets stabilize — a strong signal for long-term ownership value.

What credit score do I need to get a warehouse business loan?

Most SBA and conventional commercial lenders prefer a personal FICO score of 680 or higher. Some alternative lenders work with scores in the 600–650 range. A stronger score means better rates, lower down payment requirements, and faster approval.

How long does it take to get approved for a warehouse loan?

Alternative and equipment financing can close in 24–72 hours. Conventional CRE loans typically take 30–60 days. SBA 7(a) and 504 loans generally run 60–90 days from application to close. Plan to start the process at least 90–120 days before your target closing date.