Introduction

For decades, commercial real estate meant one of four things: office, retail, industrial, or multifamily. These traditional pillars shaped how investors allocated capital, how lenders underwrote deals, and how portfolios were built. That picture has changed substantially.

Sectors once considered niche — data centers, senior housing, self-storage, manufactured housing, single-family rentals — have moved into mainstream institutional holdings. According to a PREA Quarterly analysis by MetLife Investment Management, alternative property types grew from just 3% of the NFI-ODCE index in 2010 to approximately 13% by early 2024.

The shift extends beyond private funds. The FTSE Nareit All Equity REITs Index now allocates roughly 58% of its weight to non-traditional sectors — a sign that alternative CRE has crossed firmly into the mainstream.

This guide breaks down which alternative CRE sectors are generating the strongest returns, what's driving that performance, and — critically — how individual investors can access opportunities that were once reserved for institutions.

TL;DR

- Alternative CRE includes all commercial property types outside office, retail, industrial, and multifamily — and most have outperformed those sectors in recent years

- Top-performing sectors include manufactured housing (11.58% trailing return), data centers (9.94%), and senior housing (9.21%) per NCREIF data

- Demand drivers are structural: aging demographics, housing affordability gaps, and AI infrastructure investment will sustain growth for years ahead

- Access has widened, ranging from publicly traded REITs to direct ownership of warehouse and storage units with residential-style financing

- Key risks include illiquidity, specialized knowledge requirements, and oversupply in select markets like self-storage

What Are Commercial Real Estate Alternative Investments?

Alternative CRE investments are commercial property types that fall outside the four traditional categories. The label "alternative" no longer means obscure or experimental — data centers run at 98.6% occupancy in primary markets, and student housing hit 92.8% leased for Fall 2024. Institutional benchmarks are catching up to reflect that reality.

How Benchmarks Are Catching Up

The NCREIF NFI-ODCE index — the primary benchmark for institutional core real estate — tells the story clearly:

- 2021: NCREIF broadened its definitions to include student housing, manufactured housing, SFR, life sciences, and medical office

- Q3 2022: NCREIF began reporting performance data on these alternative sub-sectors

- April 2024: Further criteria changes revised the 75%/25% property type policy test to reflect expanded definitions

The public markets tell a similar story. As of April 2026, per the FTSE Nareit All Equity REITs Index factsheet, non-traditional sectors now account for the majority of index weight:

| Sector | Index Weight |

|---|---|

| Health Care | 17.58% |

| Data Centers | 14.10% |

| Telecommunications | 9.81% |

| Self-Storage | 6.11% |

| Manufactured Homes | 1.93% |

| Single Family Homes | 1.90% |

| Non-traditional total | ~57.8% |

Who Can Invest

Historically, alternative CRE was dominated by institutional capital and accredited investors. That's shifting. Individual investors now have access through:

- Publicly traded REITs — Welltower, Extra Space Storage, and similar funds with no accreditation requirement

- Crowdfunding platforms — Fundrise starts at $10; CrowdStreet targets accredited investors at $25,000 minimums

- Direct ownership — ownable commercial units like Personal Warehouse's warehouse condominiums, available with SBA financing or residential-style loan terms

Why CRE Alternative Investments Are Outperforming Traditional Assets

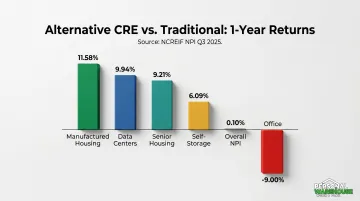

The performance gap between alternative and traditional CRE sectors has become difficult to ignore. The most recent NCREIF NPI data makes the case plainly:

| Property Type | Trailing 1-Year Return (Q3 2025) |

|---|---|

| Manufactured Housing | 11.58% |

| Data Centers | 9.94% |

| Senior Housing | 9.21% |

| Self-Storage | 6.09% |

| Overall NPI | Sub-zero (varied by sub-sector) |

| Office | Deeply negative |

Demographic Tailwinds

Two demographic forces are creating durable demand that office and retail simply can't replicate:

- Aging population: By 2030, all baby boomers will be 65 or older. The U.S. 65+ population reached 61.2 million in mid-2024 and is projected to hit 71 million — one in five Americans — by 2030. Senior housing sits directly in the path of this demand wave.

- Millennial renters: With 74 million millennials and a median first-time homebuyer age of 38, the single-family rental market has years of structural demand ahead. Many millennials who want suburban living aren't buying — they're renting.

Digital Infrastructure Demand

CBRE's North America Data Center Trends H2 2025 report documents what may be the strongest demand cycle in any CRE sector:

- Net absorption hit a record 2,497.6 MW in 2025, up from 1,809.5 MW the prior year

- Vacancy fell to a record-low 1.4% despite a 36% year-over-year increase in supply

- Rental rates for large requirements rose 12.5% year-over-year; in some markets, asking rents surged 54% over eight months

The Stargate project (OpenAI, Oracle, SoftBank) alone plans approximately 7 GW of capacity, and BlackRock's $40 billion acquisition of Aligned Data Centers signals that institutional capital is treating data infrastructure as a core — not alternative — asset class.

Needs-Based Resilience

The data center surge, senior housing growth, and self-storage stability share a common thread: they serve essential, non-discretionary needs. Housing, healthcare, data infrastructure, and storage don't pause during recessions. Self-storage was the only REIT sector to maintain positive total returns during the 2008 financial crisis, while office and retail — tied to discretionary corporate and consumer spending — continue to face structural headwinds.

Key Types of Commercial Real Estate Alternative Investments

Data Centers and Digital Infrastructure

Data centers have become one of the highest-returning CRE categories by a wide margin. The 9.94% trailing one-year return in NCREIF data reflects a sector with near-zero vacancy and rent growth accelerating faster than inflation. Cell towers and fiber optic networks fall under the broader digital infrastructure umbrella, though these are primarily accessible through specialized REITs like American Tower.

The supply constraint here is structural: power procurement and permitting bottlenecks limit new development regardless of capital availability. JLL projects global data center capacity could reach 200 GW by 2030 — meaning demand is likely to outpace new supply through the end of the decade.

Self-Storage and Warehouse Ownership

Self-storage's recession resilience is well-documented, but investors need a complete picture:

Strengths:

- Only REIT sector with positive total returns during the 2008 crisis

- Revenue grew through COVID-19 while nonresidential building lessors saw a 5.6% revenue decline in 2020

- Over 2.1 billion square feet of national inventory with net absorption of ~30 million square feet in 2024

Current headwinds:

- Post-pandemic oversupply in select markets has pressured rental rates and occupancy

- Deep discounts were required to drive 2024 absorption volumes — a sign of softening pricing power in some metros

With supply constrained and demographic demand accelerating, the sector's near-term outlook remains compelling.

Student housing presents a more mixed picture. Occupancy at core universities sits at 92.8%, but enrollment trends and location risk vary widely:

- Strong universities in growing metros continue to attract stable demand

- Overall enrollment has dipped modestly (39% in 2022 versus 41% a decade earlier)

- Smaller schools in declining regions carry meaningful vacancy risk

Single-Family Rentals and Manufactured Housing

Manufactured housing led all NCREIF NPI property types with a 3.66% quarterly return and 11.58% annual return as of Q3 2025. Zoning restrictions limiting new community development keep supply chronically constrained while demand grows steadily — a dynamic that has consistently supported returns across market cycles.

Single-family rentals are still early in institutionalization. Institutional investors own less than 5% of SFR properties and roughly 0.35% of total U.S. housing stock. NCREIF-tracked SFR fund values reached $7.5 billion in Q2 2025, up 39% year-over-year , suggesting substantial runway remains for the sector.

Benefits and Risks of Alternative CRE Investments

Benefits

- Portfolio diversification: Private real estate has historically shown a 0.04 correlation to the S&P 500 over a 20-year period — far lower than most asset classes

- Inflation hedging: Tangible asset ownership with rent escalation potential protects purchasing power over time

- Long-term demand trends: Demographics, digitalization, and housing affordability are multi-decade tailwinds not subject to business cycle fluctuations

- Income plus appreciation: Many alternative CRE investments generate rental income and capital appreciation simultaneously

Risks and Challenges

Those benefits come with real tradeoffs. Investors should weigh these risks carefully:

- Specialized knowledge: Sectors like life sciences or healthcare require operator-level understanding of regulatory frameworks, licensing, and tenant requirements

- Illiquidity: Private ownership positions can't be exited quickly; most transactions require months of marketing and due diligence

- Oversupply risk: Self-storage illustrates how low barriers to entry can erode returns even in a needs-based sector — national figures can mask serious metro-level oversupply

- Valuation complexity: Thin transaction comp sets make accurate valuations harder than in established sectors with deep market data

Due diligence for alternative CRE should meet traditional CRE standards — then go further. Before committing capital, make sure to:

- Research the operator's track record in the specific asset class

- Confirm sector-specific demand drivers hold in the target market (not just nationally)

- Assess exit liquidity for the asset type and deal structure

How to Start Investing in CRE Alternatives

The right entry point depends on your available capital, risk tolerance, and how hands-on you want to be.

| Access Channel | Typical Minimum | Accreditation Required? |

|---|---|---|

| Publicly traded REITs | Price of one share (~$50–$200) | No |

| Fundrise (crowdfunding) | $10 | No |

| CrowdStreet | $25,000 | Yes |

| Direct property ownership | Varies by project | No |

The Direct Ownership Path

For investors who want equity in a physical commercial asset — not just fund exposure — direct ownership of warehouse or storage units offers a concrete alternative. Personal Warehouse structures its units as purchasable condominiums, with SBA 504 and 7(a) financing eligibility and a 99-year ground lease that removes the land cost burden while preserving resale and leasing rights. Preferred lender programs offer residential-style loan terms — a significant advantage over traditional commercial financing.

Available unit types include:

- Flex warehouse and micro flex warehouse spaces

- Garage condos and car condos

- Professional work suites

Each unit supports customizable mezzanines, HVAC, private restrooms, and 100/150-amp 3-phase electric service. Buyers can hold, lease, or sell — with consistent leasing demand and documented resale value making these units functional as long-term investments.

Projects are currently active or accepting reservations in Montana, with pipeline activity across Colorado, Florida, Georgia, Michigan, North Carolina, Pennsylvania, South Carolina, Texas, and Wisconsin.

Tax Planning Is Not Optional

CRE alternative investments carry meaningful tax advantages — but only if you plan for them:

- 1031 exchanges: Like-kind exchange treatment applies to real property held for investment or business use, per IRS Publication 544. Commercial warehouse units, manufactured housing communities, and data centers all qualify as real property

- Cost segregation: A study can reclassify components from 39-year to 5-, 7-, or 15-year depreciation schedules, accelerating deductions in early ownership years

- Standard depreciation: Commercial property depreciates on a 39-year schedule, providing consistent annual deductions even without a cost segregation study

Before committing capital, consult both a real estate attorney and a tax advisor — outcomes vary based on your income level, holding period, and how you use the property.

Frequently Asked Questions

What is the 3-3-3 rule in real estate?

The 3-3-3 rule is an underwriting framework covering three years of financials, three comparable properties, and three professional opinions before purchasing. Its exact application varies by investor and context, so use it as a starting point rather than a rigid formula.

What is the difference between traditional and alternative commercial real estate investments?

Traditional CRE covers office, retail, industrial, and multifamily properties. Alternative CRE includes everything else — data centers, self-storage, senior housing, manufactured housing, student housing, life sciences, and more. The key distinction is that alternatives are typically driven by demographic or technological demand rather than general business cycles.

Are commercial real estate alternative investments only accessible to institutional investors?

No. While institutions and accredited investors historically dominated this space, individuals can now access alternative CRE through publicly traded REITs, crowdfunding platforms like Fundrise (starting at $10), and direct ownership programs that offer commercial properties with residential-style financing terms.

How do self-storage and warehouse spaces perform as alternative investments?

Self-storage posted positive returns through the 2008 financial crisis and held up through COVID-19, proving its needs-based resilience. Direct ownership of warehouse units can generate rental income and appreciation — tangible assets that tend to hold value during inflation. Post-pandemic oversupply is a risk in some markets, so local supply analysis matters.

What tax advantages come with owning commercial real estate alternatives?

CRE alternatives may qualify for several tax advantages:

- Depreciation deductions on a 39-year commercial property schedule

- Cost segregation to accelerate deductions over 5–15 years

- 1031 exchange treatment to defer capital gains when reinvesting proceeds

Actual outcomes depend on your tax situation, holding period, and investment structure.

How much capital do I need to start investing in commercial real estate alternatives?

Publicly traded REITs require as little as one share. Fundrise starts at $10 for non-accredited investors. CrowdStreet targets accredited investors at $25,000 minimums. Direct property ownership varies by project, but programs like Personal Warehouse offer SBA financing and residential-style loan terms that lower the effective barrier to entry well below traditional commercial real estate thresholds.