Introduction

Most industrial real estate investors spend hours analyzing cap rates, vacancy rates, and lease terms — then leave thousands of dollars on the table by ignoring the tax code.

The IRS offers commercial property owners a powerful set of deductions: accelerated depreciation, fully deductible mortgage interest, and indefinite capital gains deferral through 1031 exchanges. Used together, these tools can substantially reduce your taxable income — sometimes dramatically enough to offset an entire year's operating costs.

None of these benefits are automatic. They require intentional planning — and investors who pursue that planning consistently keep more of what their properties earn. Understanding cost segregation, bonus depreciation, and passive loss rules is often the difference between a good investment and a great one.

This guide covers each major benefit in detail: how depreciation and cost segregation work, when bonus depreciation applies, how 1031 exchanges defer capital gains, and how passive loss rules affect your overall tax position.

TL;DR

- Cost segregation can front-load industrial property depreciation into Year 1, rather than spreading it across 39 years

- Mortgage interest and operating expenses are fully deductible against rental income, with no residential-style caps

- 1031 exchanges defer capital gains taxes indefinitely, and heirs can eliminate the liability through a step-up in basis

- Bonus depreciation (currently 40% in 2025, dropping to 20% in 2026) applies to short-lived components common in industrial buildings

- Tax structuring decisions made at acquisition determine whether returns are average or exceptional

What Is Industrial Real Estate for Tax Purposes?

The IRS classifies warehouses, distribution centers, manufacturing facilities, flex spaces, and self-storage units as nonresidential real property under IRC Section 168(c). That means a 39-year straight-line depreciation schedule — notably longer than the 27.5-year schedule for residential rental property.

| Property Type | IRS Classification | Depreciation Period |

|---|---|---|

| Warehouses, distribution centers, manufacturing facilities, flex spaces, self-storage units | Nonresidential real property | 39 years |

| Apartment buildings | Residential rental property | 27.5 years |

Industrial properties fail the IRS's 80% dwelling unit test — the threshold that determines residential classification. Without qualifying dwelling units, the 39-year schedule applies by default.

That "by default" qualifier matters. The 39-year baseline is where most investors stop. Investors who plan ahead treat industrial ownership as a tax strategy from the start: long-term NNN leases reduce management obligations, while IRS-recognized depreciation rules generate paper losses that offset real taxable income.

Key Tax Benefits of Investing in Industrial Real Estate

Depreciation Deductions and Cost Segregation

Depreciation is the foundation of industrial real estate's tax efficiency. Every year, investors deduct a portion of the building's cost (land excluded) against rental income , a paper loss that requires no cash outlay. On a $3 million warehouse, the annual straight-line deduction over 39 years is roughly $77,000 per year.

Cost segregation makes that baseline deduction far more powerful.

A cost segregation study reclassifies components of an industrial building from the 39-year schedule into shorter MACRS categories:

| MACRS Period | Qualifying Industrial Components |

|---|---|

| 5-year | Specialty electrical systems, process piping, security systems, specialized lighting |

| 7-year | Office furniture, equipment not otherwise classified |

| 15-year | Parking lots, landscaping, loading dock paving, fencing, signage |

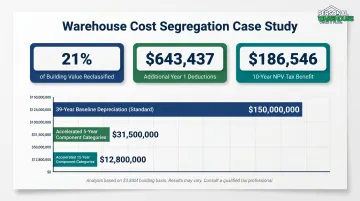

According to a KBKG warehouse cost segregation case study, a 72,700-square-foot industrial building with a $3.83M basis had 21% of its value reclassified to 5-year and 15-year categories — generating $643,437 in additional Year 1 deductions and a 10-year NPV tax benefit of $186,546. An analysis of over 8,000 cost segregation studies puts the typical industrial reclassification range at 12–25% of building basis.

Front-loading deductions improves after-tax cash flow exactly when investors need capital most — in the early years of ownership. The benefit is greatest for investors acquiring large assets, those in higher tax brackets, and those planning to hold for 5–10 years before a 1031 exchange. Commissioning the study at acquisition, not years later, captures the maximum deduction.

Mortgage Interest and Operating Expense Deductions

Interest on loans used to acquire or improve industrial real estate is fully deductible against rental income with no dollar cap , unlike residential mortgages, which are capped at interest on $750,000 of acquisition debt under TCJA rules. For leveraged industrial investments, this distinction is significant.

The IRS 2025 Schedule E instructions confirm that deductible rental property expenses include:

- Mortgage interest

- Property taxes

- Insurance premiums

- Repairs and maintenance

- Property management fees

- Legal and accounting fees

- Advertising costs for tenant placement

- Utilities (when paid by the landlord)

A simple example: An investor collects $120,000 in annual gross rent from an industrial unit. They pay $55,000 in mortgage interest and $18,000 in operating expenses. Before depreciation, taxable income is already reduced to $47,000 — a 61% reduction from gross rent.

NNN (triple net) leases, standard in industrial real estate, push property taxes, insurance, and maintenance costs onto tenants. This reduces the investor's out-of-pocket expenses while they still claim depreciation on the building and deduct whatever costs they do bear.

Investors using financing capture the most value here. Higher loan balances generate larger interest deductions, making leveraged acquisitions particularly tax-efficient compared to all-cash purchases.

Capital Gains Deferral Through 1031 Exchanges

When an industrial property is sold at a gain, IRC Section 1031 allows the investor to reinvest the proceeds into a like-kind property without paying capital gains tax at the time of sale. Industrial-to-industrial exchanges qualify. So does exchanging a warehouse for a distribution center, or any other investment real property.

The IRS timelines are strict:

- 45 days from the sale to identify replacement property

- 180 days from the sale to close on the replacement

Miss either window, and the entire gain becomes taxable in the year of sale (no exceptions outside of federally declared disasters).

The compounding math is straightforward. At the 20% long-term capital gains rate, a $500,000 gain triggers a $100,000 federal tax bill — plus the 3.8% Net Investment Income Tax for higher earners. A 1031 exchange keeps that $100,000 working in the portfolio instead.

Chain multiple 1031 exchanges over a career and the deferred amount compounds significantly. Investors who hold industrial property until death may pass it to heirs with a step-up in basis to fair market value under IRC Section 1014 , permanently eliminating the accumulated capital gains and depreciation recapture that built up over decades.

When it matters most: Investors who have held property through significant appreciation, those upgrading to larger facilities, and those actively scaling a portfolio. The step-up strategy makes 1031 exchanges not just a tax deferral tool but a potential estate planning mechanism.

Industrial-Specific Tax Advantages That Set This Asset Class Apart

Beyond the core deductions, industrial properties carry several tax advantages tied specifically to the nature of the asset.

Bonus Depreciation Under TCJA

Bonus depreciation allows investors to immediately expense a large percentage of the cost of qualified property — meaning MACRS assets with recovery periods of 20 years or less. That means cost segregation components (5-year, 7-year, and 15-year property) qualify. The 39-year building shell does not.

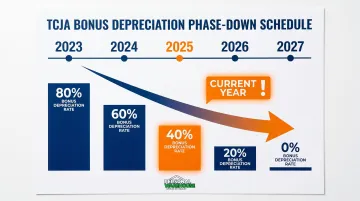

The current phase-down schedule:

| Tax Year | Bonus Depreciation Rate |

|---|---|

| 2023 | 80% |

| 2024 | 60% |

| 2025 | 40% |

| 2026 | 20% |

| 2027 | 0% (full phaseout) |

President Trump has proposed restoring 100% bonus depreciation retroactive to January 20, 2025, but legislation remains pending as of mid-2026. Each year of delay reduces the available deduction, so timing matters.

Passive Activity Loss Rules and Real Estate Professional Status

Depreciation losses from industrial properties are generally classified as passive losses, which can offset passive income from other rental properties. For investors with no passive income to offset, these losses get suspended — technically accrued but unusable until the property is sold.

The exception is the real estate professional designation under IRC Section 469(c)(7). Qualifying requirements:

- More than 50% of personal services performed in real property trades or businesses

- More than 750 hours annually in those activities

- Material participation in each rental activity

This designation removes the passive classification, allowing depreciation losses to offset W-2 wages or business income directly. For full-time investors or small business owners who actively manage their properties, it can be worth tens of thousands of dollars annually. Investors who don't qualify may still access a $25,000 special allowance — available to active participants, phasing out between $100,000 and $150,000 modified AGI.

Opportunity Zones

Industrial projects in designated Opportunity Zones qualify for additional tax benefits. The OZ regime was permanently extended by Public Law 119-21 (2025 Tax Law). Post-2026 investments receive a 5-year deferral with a 10% basis step-up, and the 10-year gain exclusion remains intact — meaning all appreciation on a Qualified Opportunity Fund investment held 10+ years can be excluded from income entirely.

New zones will be redesignated every 10 years starting January 1, 2027, with at least 25% of designated tracts required to be rural areas.

What Happens When You Ignore the Tax Strategy Side

Tax-blind industrial investing has a measurable cost. On a $3.83M property, skipping a cost segregation study means forfeiting $643,437 in Year 1 deductions — and over $186,000 in 10-year NPV. That capital, sitting with the IRS rather than reinvested, compounds against the investor's portfolio for years.

Three specific failure points are worth understanding:

Missing the 1031 exchange window can cost the full gain. If a qualified intermediary isn't in place before the sale closes, the exchange fails entirely. Proceeds become taxable income in the year of sale — no retroactive deferral is possible. The 45-day identification and 180-day closing deadlines are statutory and cannot be extended by negotiation or oversight.

Letting passive losses pile up unseen is a slower drain. Investors who don't plan for PAL rules may accumulate years of depreciation deductions that sit suspended — only accessible when the property sells in a fully taxable transaction. Early structuring prevents this: the real estate professional designation, grouping elections, and entity structure choices all open the door to active use.

Holding property in the wrong entity creates problems at exit. Investors who acquire industrial properties in their individual names, rather than through an LLC or partnership, often lose liability protection, installment sale flexibility, and the ability to transfer interests without triggering a full taxable event.

How to Maximize Your Industrial Real Estate Tax Benefits

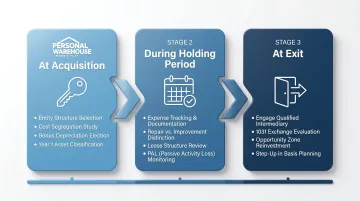

Tax benefits from industrial property don't accrue automatically — they require planning at three distinct stages:

At acquisition:

- Choose an entity structure (LLC, partnership) appropriate to your situation

- Commission a cost segregation study before or immediately after closing

- Elect bonus depreciation on qualifying short-lived components

- Confirm the property's classification and begin depreciation in Year 1

During the holding period:

- Track all deductible operating expenses systematically

- Distinguish repairs (immediately deductible) from capital improvements (depreciated over time)

- Review lease structures annually — NNN arrangements shift costs to tenants while preserving your depreciation benefits

- Monitor PAL utilization and assess whether the real estate professional designation applies

At exit:

- Engage a qualified intermediary before any sale transaction closes

- Evaluate 1031 exchange options, including upleg properties that continue the portfolio's growth

- Consider Opportunity Zone reinvestment for gains where the 10-year hold makes sense

- Factor in step-up in basis planning for estate purposes

Working with a CPA who focuses on commercial real estate — not a generalist — is the most direct way to execute this correctly. Cost segregation studies, bonus depreciation elections, and PAL rule applications each involve technical IRS compliance that generalist advisors frequently miss.

For investors who want industrial property exposure without managing a large warehouse facility, owning a smaller unit is a practical entry point. Personal Warehouse, for example, offers ownership-structured units with SBA 504 and 7(a) financing — and built-in components like mezzanines, HVAC systems, and specialty flooring that a cost segregation specialist can evaluate for potential reclassification.

Confirm the specific tax treatment with your advisor based on your unit structure and ownership arrangement.

Frequently Asked Questions

What are the most overlooked tax breaks for industrial real estate investors in the USA?

Cost segregation studies, bonus depreciation on short-lived components, and the real estate professional designation rank among the most commonly missed. None apply automatically — all require proactive planning — which is why investors working with generalist advisors frequently never claim them.

What are the 2% and 7% rules in commercial real estate investing?

These are investor screening benchmarks, not IRS rules. The 2% rule holds that monthly rent should equal at least 2% of purchase price; the 7% rule targets annual net returns of at least 7%. Neither governs tax treatment directly, but both affect how meaningfully deductions improve your after-tax returns.

How does depreciation work for industrial real estate specifically?

Industrial buildings depreciate over 39 years under standard IRS rules. A cost segregation study can reclassify components — HVAC, electrical systems, flooring, parking lots — into 5- to 15-year schedules, generating substantially larger deductions in the early years of ownership.

Can I use a 1031 exchange to swap one industrial warehouse for another?

Yes. Industrial-to-industrial exchanges qualify as like-kind under IRS rules. You must identify a replacement property within 45 days of closing the sale and complete the purchase within 180 days — both deadlines are statutory and non-negotiable.

Do I need to be a real estate professional to claim industrial real estate tax deductions?

No. Standard depreciation, mortgage interest, and operating expense deductions are available to all investors regardless of designation. The real estate professional status (750+ hours annually in qualifying activities) goes further — it removes the passive activity loss cap so depreciation losses can offset ordinary income like wages.

Is rental income from industrial properties taxed differently than wages?

Industrial rental income is typically classified as passive income and reported on Schedule E — meaning it's not subject to self-employment tax (15.3%). After depreciation and expense deductions are applied, taxable rental income is often substantially lower than the gross rent collected.