Introduction

Self-storage and office space both generate recurring commercial income — but their risk profiles, revenue mechanics, and management demands are almost nothing alike. For investors deciding between the two, those differences translate directly into long-term returns.

The numbers tell a stark story. U.S. office vacancy hit 18.6% in Q1 2026, nearly double pre-pandemic baselines of roughly 12–13%. Meanwhile, self-storage occupancy held at 92.1% through Q3 2024 and REIT-level occupancy remained at 90.4% through Q4 2025 — a sector that held above 88% occupancy even during 2020.

Choosing the wrong asset type shapes more than monthly cash flow. It locks in your exposure to vacancy risk, capital expenditure cycles, and management overhead for years.

This guide compares both asset classes across revenue per square foot, profit margins, occupancy stability, and operating costs — so you can make that call with clear data.

TL;DR

- Self-storage delivers 65–74% NOI margins versus 45–57% for office — a structural advantage driven by low staffing and zero tenant improvement costs

- Office generates 2–2.5x higher gross revenue per square foot ($37.21 vs. ~$15–18/sq ft/year), but vacancy losses and capital costs erode that lead

- Self-storage occupancy runs 88–93%; office vacancy sits at 18.6% nationally

- Lower overhead and recession-resistant demand make self-storage the stronger net-return play in most markets

- Owning storage space outright (vs. leasing) builds equity and appreciation that rental income alone can't match

Self-Storage vs. Office Space: Quick Comparison

| Metric | Self-Storage | Office Space |

|---|---|---|

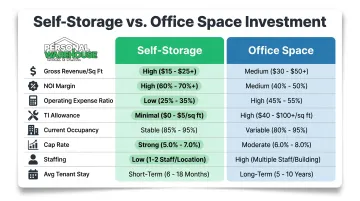

| Gross revenue/sq ft/year | $15–$18 | $33–$37 |

| NOI margin | 65–74% | 45–57% |

| Operating expense ratio | ~35% | 35–55% |

| TI allowance per lease | $0 | $87.51/sq ft (2024) |

| Current occupancy | 88–93% | ~81.4% (18.6% vacant) |

| Avg cap rate | 5.8% | Higher; widening spreads |

| Staffing per property | 3.5 employees | Significantly higher |

| Avg tenant stay | 14–24 months | Multi-year leases typical |

Revenue Per Square Foot

Self-storage nationally averages $1.26/sq ft/month for standard units and $1.47/sq ft/month for climate-controlled — roughly $15–$18 annually. Office asking rents average $37.21/sq ft/year nationally (CBRE Q1 2026), with taking rents at $33.35 after concessions.

Office wins on gross revenue per square foot. But that headline number requires three adjustments: an 18.6% vacancy haircut, tenant improvement allowances averaging $87.51/sq ft per lease cycle, and operating expense ratios that run 35–55% versus self-storage's ~35%. Once you apply those, the net return gap narrows considerably — and flips in many secondary markets.

Profit Margins

Self-storage facilities nationally operate at a 34.68% expense ratio, implying NOI margins around 65%. REIT-scale operators push that to 69–74%. Office buildings, by comparison, carry expense ratios of 35–55%, with effective NOI margins landing at 45–57% before TI allowances and leasing commissions.

That TI line is where office returns quietly erode. Office landlords spent an average of $87.51/sq ft on tenant buildouts in 2024 — a recurring cost that resets with every new lease. Self-storage operators spend zero.

Occupancy Stability

Self-storage occupancy peaked at ~94.5% during the pandemic and has normalized to the low 90s — still well above pre-pandemic baselines of ~91.5%. Office vacancy climbed from pre-pandemic levels of ~12–13% to 18.6% overall (CBRE Q1 2026), with broader availability measures reaching 22.5%.

The turnover math tells the story: when a self-storage tenant leaves, the unit re-rents within days at minimal cost. When an office tenant leaves, expect months of vacancy plus a full TI buildout before the next tenant moves in.

Management Intensity

Self-storage employs an average of 3.5 people per facility across more than 50,000 U.S. locations. Smart access systems, online booking, and automated billing make semi-absentee operation realistic for most owners — a meaningful advantage for investors who aren't looking to run a full-time business.

Office properties carry a heavier operational load:

- Property management teams and engineering staff on-site

- Janitorial services and dedicated security

- Ongoing tenant relations and unit modifications

- Lease renegotiations every 3–10 years, each triggering new TI costs

What Is Self-Storage Revenue?

Self-storage is among the most recession-resilient forms of commercial real estate. Rentable units range from small 5×5 spaces to large 10×30+ bays, with individuals and businesses paying month-to-month for secure access.

Core Revenue Streams

Revenue doesn't stop at monthly unit rentals. Strong operators layer in:

- Tenant protection plans — insurance programs that add recurring revenue per occupied unit

- Retail sales — locks, boxes, and moving supplies at the point of rental

- Vehicle, RV, and boat storage — larger units command premium rates; over 9% of the market uses 10×30 bays for vehicle storage

- Climate-controlled premiums — CC units generate $1.47/sq ft/month versus $1.26 for standard units

- Late and administrative fees — small per-unit amounts that compound across large portfolios

Revenue Benchmarks

A 50,000 sq ft self-storage facility at 90% occupancy and $1.26/sq ft/month generates approximately $680,000 in annual rental revenue. At climate-controlled rates, that rises to roughly $794,000. Average national move-in rates across all unit types ran $96.44/month in late 2025, reflecting competitive discounting — though in-place tenant rates are typically higher.

Location shapes these numbers dramatically. A standard 10×10 in San Francisco or New York commands $296–$302/month; the same unit in a secondary market might fetch $80–$120.

The Ownership Advantage

Beyond rental income, investors who own storage facilities rather than lease them capture a second return stream: asset appreciation.

Personal Warehouse structures this through an ownership model where buyers acquire warehouse-style spaces using SBA 504 or 7(a) financing on terms comparable to residential loans, secured by a 99-year ground lease. That structure lets buyers build equity without bearing the full cost of land acquisition — a concrete advantage in high-growth markets like Bozeman, MT, where the company's first project is under construction and accepting reservations.

Who Drives Self-Storage Demand

- Moving and relocation — 31% of renters use storage during moves (StorageCafe 2025)

- Home space constraints — 35% cite lack of space at home as the primary driver

- Downsizing — 8% are transitioning to smaller living arrangements

- Business storage — inventory, equipment, and operational supplies

- RV, boat, and vehicle owners — a growing segment preferring covered, secure storage over exposed lots

That spread across five distinct demand drivers means no single customer type can meaningfully move the occupancy needle on its own.

What Is Office Space Revenue?

Office space breaks into three tiers: Class A (premium urban), Class B (suburban or older urban), and flex/coworking. Revenue is generated through leases that typically run 3–10 years, with tenants paying per square foot annually.

Revenue Benchmarks

National average asking rents sit at $37.21/sq ft/year, with taking rents at $33.35 after concessions (CBRE Q1 2026). The 10.4% spread between asking and taking rents — wider than the pre-pandemic 8.6% gap — signals that landlords are still negotiating hard to close deals.

Secondary and tertiary markets trail national averages sharply. Colorado Springs, for example, carries a direct asking rent of $17.71/sq ft NNN (CBRE H2 2025) — less than half the national figure and competitive with self-storage gross revenue on a per-square-foot basis.

Post-Pandemic Revenue Risk

The structural shift toward hybrid and remote work has significantly shifted office demand in many submarkets. Key data points:

- National office vacancy: 18.6% overall, 12.7% for prime assets (CBRE Q1 2026)

- Leasing activity remains at only 82% of pre-pandemic levels (JLL Q3 2025)

- Net absorption turned positive for eight consecutive quarters, but gains are concentrated in premium urban assets

- Office completions hit just 1.3M sq ft in Q1 2026 — the lowest quarterly figure since 1990

The market has split sharply: Class A in dense urban cores is recovering. Suburban Class B is not.

When Office Space Outperforms

Office space makes sense in specific conditions:

- Prime urban locations with low vacancy and strong corporate tenant demand (Midtown Manhattan prime vacancy: 2.9%)

- Medical office and lab/flex space — higher-yield niches with specialized demand that outpaces general office

- Long-term creditworthy tenants — when secured, office leases provide income visibility that self-storage's month-to-month structure can't match contractually

Office can outperform self-storage on a per-square-foot basis — but only with the right location and tenant locked in. Without both, vacancy periods and tenant improvement (TI) costs can erode that advantage quickly, turning a premium-looking deal into a break-even proposition.

Self-Storage vs. Office Space: Which Generates More Revenue?

Neither asset type is categorically superior. Revenue outcomes depend on market conditions, asset quality, and operational execution. That said, the data points in a clear direction for most investors.

Revenue Resilience Through Economic Cycles

Self-storage occupancy stayed above 90% through both the 2008 recession and the COVID-19 pandemic. Office vacancy surged during both. According to CBRE's Q1 2026 office market report, overall vacancy is still 18.6% — more than five years after the pandemic began, with no full recovery in sight for most markets.

Self-storage's month-to-month lease structure, is a stability feature rather than a weakness. A broad customer base of hundreds of individual tenants absorbs individual move-outs without meaningful revenue disruption.

Revenue Efficiency: NOI and Margins

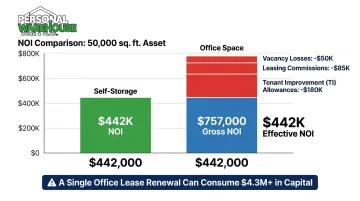

For a 50,000 sq ft asset at comparable occupancy:

- Self-storage at 90% occupancy, $1.26/sq ft/month, 65% NOI margin → ~$442,000 NOI

- Office at 81.4% occupancy, $37.21/sq ft/year, 50% NOI margin (before TI) → ~$757,000 NOI — but subtract TI allowances of $87.51/sq ft on lease cycles, leasing commissions, and extended vacancy periods

For a 50,000 sq ft office building, a single lease renewal with full TI buildout can consume $4.3M+ in capital — a cost self-storage investors never face.

Situational Recommendations

Choose self-storage if:

- You're investing in suburban or secondary markets

- You want lower management overhead and minimal staffing

- You prefer demand diversification over long-term lease contracts

- You don't have the capital base for Class A office build-outs

- You want to own — not just operate — an appreciating physical asset

Choose office space if:

- You have access to a prime urban location with confirmed corporate tenant demand

- You can secure long-term leases with creditworthy tenants

- You're prepared for active management and recurring TI capital outlays

The Hybrid Opportunity

Some operators are capturing revenue from both categories by combining light industrial storage with flexible workspace — without the TI exposure or tenant concentration risk of traditional office. Personal Warehouse is built around this model, offering ownership units that can function as storage, fabrication studios, professional work suites, or creative offices depending on the buyer's needs. Each unit is designed to support both use cases from day one:

- 100/150-amp 3-phase electrical service for tools, equipment, or workstations

- Insulated overhead doors and all-LED lighting standard

- Optional mezzanines that expand usable square footage by up to 30%

Buyers can hold, lease, or sell — capturing revenue from storage and workspace markets without the capital drag of office TI buildouts.

Real-World Scenario: How the Numbers Play Out

To make this concrete, consider a side-by-side comparison of a 10,000 sq ft self-storage facility versus a 10,000 sq ft suburban office property in a market like Colorado or Texas.

| Metric | Self-Storage (10,000 sq ft) | Suburban Office (10,000 sq ft) |

|---|---|---|

| Gross rent/sq ft/year | $15.12 (non-CC avg) | $17.71 (CO Springs NNN avg) |

| Effective occupancy | 90% | 81.4% |

| Gross revenue | ~$136,000 | ~$144,000 |

| Operating expense ratio | 35% | 45% |

| Operating expenses | ~$47,600 | ~$64,800 |

| NOI before TI | ~$88,400 | ~$79,200 |

| TI allowance (amortized) | $0 | ~$21,900/year* |

| Effective NOI | ~$88,400 | ~$57,300 |

*TI allowance of $87.51/sq ft amortized over a 4-year average lease cycle

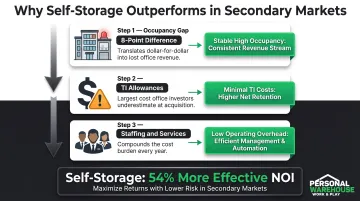

In this secondary market comparison, self-storage produces 54% more effective NOI despite similar gross revenue. Lower operating costs and zero TI capital requirements account for the entire gap.

Three variables drive that outcome most directly:

- An 8-point occupancy gap between self-storage and office translates dollar-for-dollar into lost revenue

- TI allowances are the largest cost office investors consistently underestimate at acquisition

- Higher staffing and service requirements in office properties compound that cost burden every year

For most investors entering without an existing tenant base or a premium urban asset, self-storage delivers more predictable revenue with significantly lower day-to-day risk. If you're weighing a storage investment and want to understand how an ownership-based model fits into these numbers, Personal Warehouse offers projects across multiple states with flexible financing through SBA 504 and 7(a) loans. Reach them at info@personalwarehouse.com or 303-222-0768.

Conclusion

Both self-storage and office space can work as investments. But they operate on fundamentally different economics, and the post-pandemic environment has widened the gap between them.

Self-storage wins on margin efficiency, occupancy stability, and management simplicity. Office space can outperform in premium urban markets with the right tenants — but that scenario describes a narrowing slice of the total market, not the norm in most U.S. cities.

That broader picture becomes even clearer at the local level. In growth markets like Montana, Colorado, and Texas, demand for flexible storage and warehouse space is consistently outpacing new supply. For investors in these regions, the monthly cash flow, NOI strength, and equity upside from owning — rather than leasing — stack up in ways that renting a traditional office suite simply cannot match. The flexibility to hold, lease out, or resell a owned unit as conditions shift adds a layer of optionality that keeps performing long after the initial purchase.

Frequently Asked Questions

What is the average revenue for a self-storage facility?

A typical 50,000 sq ft self-storage facility at ~90% occupancy generates approximately $680,000–$794,000 in annual rental revenue, depending on unit mix and climate-control penetration. Size, location, and local supply dynamics significantly affect actual results.

Can you write off a storage unit on taxes for a business?

Businesses renting storage units for inventory, equipment, or operational purposes can generally deduct the cost as a business expense. Consult a qualified tax professional for guidance specific to your situation and business structure.

Can you use a self-storage unit as an office?

Traditional self-storage units are typically not zoned or designed for occupied workspace use. Personal Warehouse's Professional Work Suites are purpose-built to serve as both active business workspaces and storage — fully designed for legal occupancy from the ground up.

How many sq ft is a 10x20 storage unit?

A 10×20 unit is 200 square feet — roughly the size of a one-car garage. It can typically hold the contents of a 2–3 bedroom home or accommodate small business inventory and equipment.

Which is more profitable: self-storage or office space?

Self-storage generally produces stronger NOI margins (65–74%) and more stable occupancy than office space in most markets, especially post-pandemic. Class A office in premium urban locations can command higher asking rents, but net returns often favor self-storage once you factor in vacancy and tenant improvement buildout costs.

What are the main risks of investing in office space compared to self-storage?

Office space's primary risks are elevated vacancy rates (18.6% nationally), high tenant improvement costs averaging $87.51/sq ft per lease, and extended lease-up periods between tenants. Self-storage carries lower entry risk, a diversified tenant base, and significantly simpler operations.