Introduction

Most investors still think of self-storage as a niche oddity — metal buildings filled with old furniture and forgotten treadmills. The numbers tell a very different story.

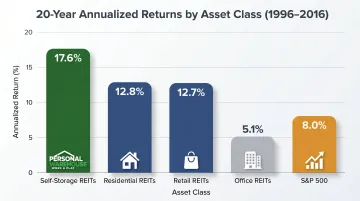

Self-storage REITs delivered 17.6% annualized returns over 20 years (1996–2016), more than double the S&P 500's 8.0% over the same period. A $10,000 investment grew to $255,687 in self-storage versus $46,410 in the broader market.

That resilience held even under pressure. During the 2008 financial crisis — when most real estate sectors lost 25% to 67% of their value — self-storage was the only REIT sector to post a positive return.

The real wealth opportunity lies in owning the real estate behind it. Whether through full facility acquisitions, direct unit ownership, or REIT shares, self-storage offers recession resilience, low overhead, and compounding returns that are genuinely hard to find elsewhere in commercial real estate.

This article breaks down the structural advantages that make self-storage worth a serious look — and how investors can get positioned.

TL;DR

- Self-storage has outperformed apartments, retail, office real estate, and the S&P 500 over a 20-year period

- Demand holds through recessions — the life events that drive storage (moving, divorce, job loss) don't pause when the economy does

- Operating expenses run just 30–35% of revenue, far below the 45–50% typical of multifamily properties

- Direct unit ownership gives investors control over pricing, improvements, and exit timing that REIT shareholders don't have

- Sun Belt and Mountain West markets lead on demand, driven by population growth and tight housing supply

What Is Self-Storage Real Estate Investing?

Self-storage investing means acquiring real estate that generates recurring rental income — either from individual units or entire facilities — while the underlying asset appreciates over time.

The entry points span a wide range:

- Publicly traded REITs — Liquid and accessible entry, but you own shares in a company, not physical property. No say in operations or asset decisions

- Full facility acquisitions — Maximum control and upside, but requires significant capital and active day-to-day management

- Direct unit ownership — Buy individual warehouse-style units as titled real property (think commercial condo). Lower capital requirement than a full facility, with real control over your specific asset

Each approach delivers the same three fundamentals investors care about:

- Cash flow from recurring tenant rents

- Asset appreciation as the underlying real estate gains value

- Diversification away from stock market volatility and traditional residential property

With 1 in 3 Americans currently renting a storage unit across a market valued at approximately $237 billion, the demand base is broad and durable.

Key Advantages of Self-Storage Real Estate

The advantages below aren't theoretical. They're grounded in NAREIT performance data, operating benchmarks, and documented market outcomes.

Recession-Resistant Demand Across Every Economic Cycle

Self-storage demand is driven by life events, not economic sentiment. Moving, downsizing, divorce, job loss, business relocation, death in the family — these happen in every economic environment. Industry practitioners refer to this as the "Six Ds":

- Dislocation (moving, relocation)

- Downsizing

- Divorce

- Death

- Distribution (e-commerce and small business use)

- Decluttering

The recession performance data is stark. According to the U.S. Census Bureau, self-storage was the only REIT sector to post a positive total return in 2008 — recording +5% while other commercial real estate segments lost between 25% and 67%.

During downturns, the demand logic reinforces itself in two directions. When people downsize from homes to apartments, they still need storage for what won't fit. When businesses cut office space, they still need inventory and equipment storage.

Job losses follow the same pattern — people move, and moving generates storage demand.

Affordability reinforces retention. A standard 10x10 non-climate-controlled unit averages $119 per month nationally — a low enough line item that most tenants keep paying even when cutting other expenses.

Why this matters for investors: More predictable monthly cash flow, lower portfolio volatility in downturns, and an asset class that historically holds occupancy when others don't. Decade-average occupancy has stayed between 90% and 93%.

Superior Returns With Minimal Operating Overhead

Self-storage facilities carry dramatically lower operating costs than other commercial real estate categories. There's no tenant improvement buildout, no per-unit plumbing or HVAC maintenance, and staffing needs are minimal — often 1 to 3 people, with modern automation reducing those requirements by 20–30% further.

Operating expenses run 30–35% of total revenue for self-storage, versus 45–50% for multifamily properties — a gap that translates directly to higher net operating income per dollar of revenue collected.

The NAREIT historical data on returns tells the same story:

| Asset Class | 20-Year Annualized Return (1996–2016) |

|---|---|

| Self-Storage REITs | 17.6% |

| Residential REITs | ~12.8% |

| Retail REITs | ~12.7% |

| Office REITs | Underperformed S&P 500 |

| S&P 500 | 8.0% |

Self-storage also shows unusual cap rate stability. During market corrections, self-storage cap rates fluctuate within a 50–75 basis point range, compared to 100+ basis points for multifamily. That stability makes valuations more predictable across cycles.

Key metrics this improves: net operating income, cap rate stability, cash-on-cash return, and operating profit margin — the figures that determine whether a deal makes sense at acquisition and holds up as you scale.

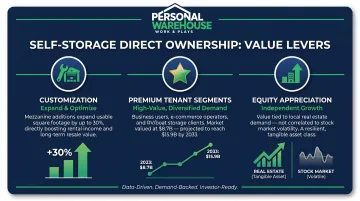

Direct Ownership: Customization, Resale Value, and Scalable Wealth

Beyond facility-level investing, individual investors can own self-storage and warehouse units as titled real property — with full decision-making authority over pricing, tenants, improvements, and exit timing that REIT shareholders simply don't have.

This ownership model opens three specific levers for building value:

- Customization — Structural additions like mezzanines expand usable square footage by up to 30%, increasing both rental income potential and resale value without acquiring a separate property

- Premium tenant segments — Business users, e-commerce sellers, RV and boat owners, and creative professionals increasingly need flexible, high-quality storage space. The U.S. RV and boat storage market alone was valued at $8.7 billion in 2024 and is projected to reach $15.9 billion by 2033

- Equity appreciation — Asset value builds independently of stock market fluctuations, tied to local demand fundamentals and property-level improvements

Personal Warehouse is built around this ownership model. Investors can purchase warehouse-style units in markets like Bozeman, MT with financing terms comparable to residential loans, backed by a 99-year ground lease structure that provides long-term stability.

Customizable mezzanines, HVAC, restrooms, and premium finishes let owners tailor their units to attract higher-paying tenants — and command stronger resale prices at exit.

Geography plays a measurable role in performance. The South accounts for 34 of the top 50 best-performing self-storage markets nationally, and the Mountain West — including fast-growing cities in Montana and Colorado — is outpacing national averages in demand intensity.

What Happens When Investors Overlook Self-Storage

Avoiding self-storage comes with a measurable cost — one that compounds over time.

The return gap is hard to ignore. A $10,000 investment in self-storage REITs in 1996 grew to $255,687 by 2016. The same amount in the S&P 500 grew to $46,410 — a 5.5x wealth gap over two decades. Every year of under-allocation makes that gap harder to close.

That return advantage doesn't exist in a vacuum. Self-storage also sidesteps structural risks that quietly drag down performance in other real estate categories:

- Lower operating costs — Residential and retail properties carry ongoing HVAC, structural, and tenant improvement expenses. Self-storage avoids most of them, protecting net returns

- Distributed vacancy risk — A single vacancy in a four-unit residential portfolio wipes out 25% of revenue. In a 100-unit storage facility, that same vacancy is less than 1% of income

- Easier incremental scaling — Adding residential or commercial properties requires substantial capital and complex transactions. Storage units can often be acquired in stages as capital becomes available

Office vacancy sat at 18.5% nationally in 2024. Multifamily fell to roughly 88% occupancy in 2023. Self-storage, by comparison, has maintained its decade-average occupancy band of 90–93% through the same period.

How to Get the Most Value from Self-Storage Real Estate

Three conditions determine whether a self-storage investment performs well over time. All three are within an investor's control.

1. Validate location and demand before committing

Not all markets perform equally. CBRE Investment Management uses a 7-variable screening framework to rank 50+ markets, weighting population growth, housing turnover, existing home sales, and projected rent growth.

Their top-rated markets skew heavily toward Sun Belt and Mountain West metros: Las Vegas, Houston, Salt Lake City, Tampa, Jacksonville, Raleigh-Durham, Phoenix, and San Antonio. Coastal markets like the Bay Area, Boston, and New York/New Jersey consistently rank near the bottom, due to low housing activity and below-average per-capita storage usage.

Screen for these red flags before committing:

- New construction adding 5–7% annual inventory without matching demand growth

- Oversaturation already depressing rents (Atlanta and Orlando are current examples)

2. Choose the right ownership structure for your goals

| Structure | Control | Capital Required | Liquidity |

|---|---|---|---|

| REIT shares | None | Low | High |

| Full facility | Maximum | Very high | Low |

| Direct unit ownership | High | Moderate | Moderate |

Direct unit ownership — the model Personal Warehouse uses — sits at a practical middle ground. Investors get real property rights, customization potential, and resale flexibility with financing structures that resemble residential mortgages, including potential SBA 504 and 7(a) loan eligibility.

3. Track the right metrics and act on them

Monitor these three KPIs on a regular cycle:

- Net operating income — signals whether cost management is working

- Occupancy rate — signals when to raise rents or adjust tenant mix

- Rental rate per square foot — signals whether premium features are generating yield

Consistent monitoring of these numbers is what separates investors who capture full upside from those who leave yield on the table.

Frequently Asked Questions

Are self-storage units a profitable investment?

Yes. Well-run facilities operate with 65–70% NOI margins, driven by operating expenses of just 30–35% of revenue. Combined with decade-average occupancy of 90–93%, self-storage is one of the more reliable income-generating categories in commercial real estate.

How much revenue can a 100-unit self-storage facility generate?

At $100 per unit per month and 85–92% occupancy, a 100-unit facility generates roughly $102,000–$110,400 in effective gross annual income. After standard operating expenses, net operating income lands in the $66,000–$77,000 range annually — though location, unit mix, and premium features all shift these figures.

What is the 7% rule in real estate investing?

The 7% rule states that a property should generate at least 7% of its purchase price in annual net returns to qualify as a strong investment. Self-storage cap rates typically range from 6.0% to 7.5%, meaning many self-storage investments meet or exceed this threshold at acquisition.

How does self-storage investing compare to traditional real estate?

Self-storage carries lower overhead (30–35% OpEx vs. 45–50% for multifamily) and requires minimal tenant management. Vacancy risk spreads across dozens or hundreds of units, and the asset class has historically outperformed residential rentals, retail, and office properties on long-term returns.

What are the biggest risks of investing in self-storage real estate?

The primary risks are market oversaturation (new construction adding 5–7% annual inventory in some regions), location-specific demand variability (coastal markets significantly underperform Sun Belt markets), and interest rate sensitivity — transaction volumes dropped approximately 35% between 2022 and 2024 as financing costs rose.

Can you buy individual storage units as a direct real estate investment?

Yes. Individual warehouse-style units can be purchased as titled real property, similar to a commercial condo — giving you direct ownership, financing access, and resale rights. Unlike REIT investing, you control the asset directly: pricing, improvements, tenant selection, and exit timing. Personal Warehouse structures its units exactly this way, with SBA-eligible financing and titled ownership from day one.