Introduction

Investor appetite for hands-off real estate income has intensified in 2026 — and self-storage keeps landing at the top of the shortlist. Three factors explain why: persistent demand regardless of economic conditions, operating margins that leave most other property types behind, and automation tools that have removed the management burden that once made real estate feel like a second job.

The catch is that self-storage is often misread as an active business rather than a passive asset. Many investors assume it means managing tenants, fielding complaints, and staying on-site — and walk away from the opportunity entirely.

That assumption is outdated. This article breaks down five concrete reasons why self-storage consistently delivers on the passive income promise, from recession-proof demand fundamentals to scalable entry points that work for investors at every capital level.

TL;DR

- Self-storage was the only REIT sector to post positive returns (+5.0%) in 2008 while equities collapsed — recession resistance isn't theoretical here

- Industry profit margins average 36%, nearly double the 22% all-industry average, driven by minimal maintenance costs

- Modern facilities run unmanned with AI pricing, digital billing, and remote access — overhead stays low because staffing is optional, not required

- Direct ownership builds real equity: self-storage has delivered 11.6% average annual returns since 2006, outpacing most asset classes

- Entry options range from REIT shares to direct unit ownership — Personal Warehouse structures purchases with financing terms closer to a home loan than a commercial real estate deal

What Is Self-Storage Passive Investment?

At its simplest: you own all or part of a storage facility (or individual units), and tenants pay monthly rent to store their belongings or business inventory. You collect income. The asset appreciates.

The spectrum of involvement is wide. On one end, REIT investors buy shares in publicly traded storage companies and never visit a facility. On the other, investors own individual units or entire facilities, with day-to-day operations handled by automated systems or third-party managers. Personal Warehouse operates in that direct-ownership segment, offering individual unit ownership with SBA-eligible financing terms structured closer to a residential purchase than a typical commercial acquisition.

What separates self-storage from residential rental is structural simplicity. The operational headaches that erode landlord returns largely don't apply here:

- No plumbing repairs or interior renovations between tenants

- No eviction proceedings: operators hold a statutory lien on stored goods, creating a legally cleaner resolution than residential landlord-tenant law

- No tenant improvements or build-outs required between occupants

Tenant turnover is also lower than most investors expect. The average tenant stay is 18.5 months, according to SpareFoot's 2026 industry data.

5 Reasons Self-Storage Is the Perfect Passive Investment in 2026

The five reasons below are grounded in operating data and structural features of the asset class — not marketing claims.

Reason 1: Demand Is Recession-Resistant and Counter-Cyclical

Self-storage demand runs on life events, not consumer sentiment. Moving, downsizing, divorce, business relocation, death of a family member — these trigger storage needs in boom years and recession years alike. The industry shorthand is the "Four Ds": death, divorce, downsizing, and dislocation.

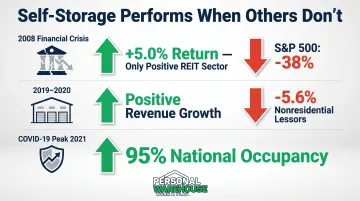

According to NAREIT data cited by the U.S. Census Bureau, self-storage was the only REIT sector to post a positive total return in 2008, achieving +5.0% while the S&P 500 fell -38% and every other REIT sector declined.

The counter-cyclical effect ran the opposite direction during COVID-19: national self-storage occupancy peaked at 95% in 2021 as remote work and household relocation drove demand to record levels.

| Event | Self-Storage Outcome |

|---|---|

| 2008 Financial Crisis | +5.0% total return (only positive REIT sector) |

| 2019–2020 (Census SAS) | Positive revenue growth vs. -5.6% for nonresidential lessors |

| COVID-19 Peak (2021) | 95% national occupancy |

One practical reason for this resilience: the average monthly storage cost runs about $129, roughly 2% of household income. That's not a budget line tenants cut during hard times. Compare that to apartments averaging $2,156/month — approximately 35% of income — and the price sensitivity gap is obvious.

For passive investors holding through a downturn, that price gap is what keeps occupancy steady when other real estate assets see tenant flight.

Reason 2: Low Overhead Creates Industry-Leading Profit Margins

Storage facilities don't have per-unit HVAC systems, plumbing, or interior finishes to maintain between tenants. Units are enclosed spaces. Turnover costs are minimal. The operational simplicity shows up directly in profit margins.

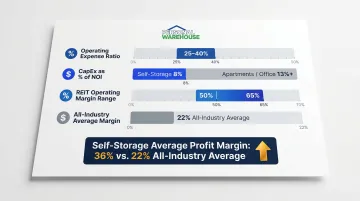

The industry average profit margin sits at approximately 36% — nearly double the 22% all-industry average. At the REIT level, operating margins run 50–65%, with Public Storage reporting a same-store NOI margin of 73.9% for full-year 2025. Capital expenditure requirements average just 8% of NOI, compared to 13% or more for apartments and office buildings.

Key margin benchmarks:

- Operating expense ratio (SSA benchmark): 25–40% of gross potential income

- CapEx as % of NOI: 8% (self-storage) vs. 13%+ (apartments/office)

- REIT operating margin range: 50–65%

- All-industry average for comparison: 22%

These metrics are predictable precisely because the cost structure is lean. No plumbing emergencies. No appliance replacements. No unit-by-unit renovation cycles eroding cash flow. The infrastructure stays simple, and the margins hold.

Reason 3: Automation Has Made Self-Storage Truly Hands-Off

The management burden that once made real estate feel like a second job has largely been automated away in modern self-storage operations. The technology stack now includes:

- Smart-lock and remote gate access — tenants enter without staff involvement

- Digital tenant onboarding — lease signing, ID verification, and payment setup handled online

- Automated billing and late-fee processing — no manual follow-up required

- AI-driven dynamic pricing — rental rates adjust in real time based on unit availability, local demand, and competitor pricing, maximizing revenue without operator intervention

Most stabilized facilities today operate with one part-time manager or a third-party management company handling oversight remotely. For passive investors, this means the asset generates income without requiring active involvement — closer to owning a dividend-paying stock than managing a rental property.