Introduction

The shared office space industry has grown far beyond its coworking roots. What started as open desks and ping-pong tables for freelancers has evolved into a sophisticated ecosystem spanning hybrid-use facilities, corporate suites, flex industrial spaces, and ownership-based models.

In 2026, that complexity matters. The U.S. market crossed 9,100 locations and 164 million square feet in Q1 — yet still represents only about 2.2% of total U.S. office inventory. That gap signals a market still in its growth phase, with significant structural shifts underway.

For small business owners, investors, and entrepreneurs, the direction this market takes has real financial stakes. Whether you're deciding to rent, buy, or something in between, workspace decisions directly shape operating costs, flexibility, and long-term asset value.

This report breaks down the five most significant trends shaping shared office space in 2026, what's driving them, and what they signal for owners and investors through 2027 and beyond.

TL;DR

- The U.S. coworking market hit 9,100+ locations and 164M sq ft in Q1 2026 — but only 2.2% of office inventory, leaving substantial room to grow

- Secondary markets like Jacksonville (+43% sq ft) and Richmond–Tidewater (+34% locations) are outpacing major metros in growth rate

- Corporate teams account for ~27.6% of coworking revenue — and ~59% of expanding companies now choose flex space over traditional leases

- AI-powered dynamic pricing is delivering 50%+ revenue increases for operators who deploy it

- Ownership-based flex space models offer a wealth-building alternative to paying rent indefinitely with no equity return

Trend 1: Secondary Markets Are Outgrowing Gateway Cities

For most of the past decade, coworking growth clustered in a handful of coastal metros — New York, San Francisco, Chicago, Los Angeles. That concentration is unwinding fast.

By early 2026, Jacksonville recorded +43% square footage growth — the highest nationally — while Richmond–Tidewater saw +34% location growth. On penetration, Las Vegas leads the country at ~3.5% of total office inventory in flex, followed by the Southwest Florida Coast at ~3.3% and West Palm Beach–Boca Raton at ~2.9%.

Why Secondary Markets Are Accelerating

Three forces are driving this shift:

- Lower land and construction costs make new flex developments financially viable in secondary metros, where gateway cities face compressed margins

- Remote-first hiring puts more workers in smaller cities who need nearby professional workspace — and need it consistently

- Previously underserved metros are now seeing their first branded flex locations, with national operators expanding alongside established independents

What This Means for Small Business Owners

If you're based in a mid-tier city, this is good news. Shared office space is becoming accessible and competitively priced in markets that had limited options just three years ago.

For operators and investors, the opportunity looks different: secondary markets are gaining penetration pace, while gateway cities are adding volume without the same growth velocity.

States like Montana, North Carolina, Colorado, and Florida — markets where Personal Warehouse is actively developing ownership-based workspace and storage facilities — sit squarely in this growth corridor.

Trend 2: Corporations Are Choosing Flex Space as Their Primary HQ

Corporate and professional users now account for ~27.6% of global coworking revenue. A WeWork-cited survey summarized by Archie found that ~59% of expanding companies prefer flex space over traditional leases. The "coworking is for freelancers" assumption no longer holds — the numbers tell a different story.

How Corporate Adoption Plays Out

In practice, this looks like:

- Companies signing 3–12 month private suite agreements instead of 5–10 year traditional leases

- Teams using flex space as a permanent HQ rather than a temporary bridge solution

- Finance, IT, and professional services firms leading adoption — sectors that need professional environments but want to avoid long-term capital commitments

The bundled cost model is a significant driver. A single monthly payment covering utilities, internet, janitorial, and IT infrastructure is far easier to manage than the fragmented expense structure of a traditional office lease.

The Ripple Effect for All Tenants

Corporate demand is reshaping the product itself. To attract enterprise clients, operators are upgrading amenities, adding private meeting suites, and raising service standards across the board. Every tenant benefits — from the solo consultant to the 20-person team.

Trend 3: AI and Technology Are Transforming Space Operations

Shared office space is becoming a data-driven business, and operators who haven't adopted AI tools are already falling behind.

The numbers are compelling. Operators using dynamic pricing tools from providers like Flexspace AI report average revenue increases of 50%+, driven by real-time price adjustments tied to demand. Automation platforms save operators 15+ hours per week in administrative work — time that previously went to manual scheduling, invoicing, and member communications.

What AI Adoption Looks Like in Practice

- Dynamic pricing engines that adjust meeting room and desk rates based on time of day, booking lead time, and occupancy levels

- AI chatbots handling tour scheduling, membership inquiries, and support tickets without staff involvement

- Occupancy sensors informing space layout decisions — operators are using real-time utilization data to convert underused open-desk areas into higher-yield private offices

- Predictive analytics that help operators optimize their product mix across desks, offices, and event spaces

Why This Is Now a Baseline Expectation

As operating costs rise and competition from new flex locations intensifies, automation is the difference between a profitable operation and one that breaks even. Operators who have already deployed AI-assisted pricing and booking tools are compounding that edge month over month — widening the gap against locations still running on manual processes.

Trend 4: Flex Industrial and Hybrid-Use Spaces Are Filling a Critical Gap

Traditional office-style coworking doesn't work for everyone. A woodworker, an e-commerce operator managing inventory, a fabricator, or a vehicle collector doesn't need a hot desk and a coffee bar — they need functional space that handles their actual operations. Flex industrial and hybrid-use formats are moving in to meet that demand.

The Demand Context

Industrial vacancy in the U.S. sits in the 5.2%–7.0% range — tight by historical standards — with asking rents running $8–$15 per square foot depending on market. Small-bay micro-flex units (typically 1,000–5,000 sq ft) that combine office and warehouse functions are in high demand and short supply.

The businesses driving this demand include:

- E-commerce operators needing last-mile storage with workspace attached

- Tradespeople and fabricators who need power, ventilation, and overhead door access

- Creative professionals — photographers, set builders, studio operators — who need industrial infrastructure with a professional finish

- Collectors protecting vehicles, art, or equipment in climate-controlled, secure facilities

The Ownership Angle

That supply gap is exactly what Personal Warehouse units are built to address. Rather than leasing a generic flex industrial unit indefinitely, small business owners can purchase a space built around their operations — and build equity instead of paying rent.

Units come standard with:

- Commercial overhead doors and 100/150-amp 3-phase electrical service

- High-efficiency insulation for climate control

- Optional mezzanines that expand usable space by up to 30%

Trend 5: Ownership Models Are Emerging as an Alternative to Monthly Leasing

At some point, perpetual rent stops making financial sense — and a growing number of small business owners and investors are running those numbers.

The ownership-based flex space model works differently than traditional commercial real estate. Instead of purchasing land outright, buyers acquire the improvements (the unit, its customizations, its infrastructure) under a long-term ground lease — typically 50 to 99 years. This structure separates the land cost from the building cost, making ownership accessible at price points closer to residential real estate than traditional commercial acquisition.

Why the Economics Are Compelling

- Small commercial warehouse units often sell in the $200,000–$500,000 range with down payments of 10–25%, depending on financing structure

- SBA 504 and 7(a) loans — available for owner-occupied commercial properties — can make financing terms comparable to residential mortgages

- Monthly ownership costs can be more predictable than open-ended leases subject to rent escalation at renewal

- Ownership creates three exit options: hold and use, lease to a third party, or sell. Traditional rental arrangements offer none of these paths.

Personal Warehouse structures its units under a 99-year ground lease — buyers own the unit and its improvements, gain resale and leasing rights, and access financing through preferred lenders experienced in SBA programs for micro-flex condominiums.

That structure mirrors patterns already proven in residential real estate and self-storage — sectors where ownership displaced perpetual renting once buyers recognized the long-term cost difference. The math tends to close the argument.

What's Driving These Shared Office Space Trends

These five trends share common roots — behavioral, economic, and structural shifts that are reshaping how businesses think about space.

Hybrid Work Has Become Permanent Infrastructure

As of 2025, approximately 51–53% of remote-capable U.S. employees work hybrid schedules, averaging 2.3 days per week in-office. Fully remote sits at 21%; fully on-site at 26%. That split isn't a transitional phase — it's the new baseline, and it's generating durable demand for distributed, meeting-capable workspace that scales with headcount rather than locking teams into fixed footprints.

Office Vacancy Is Pushing Tenants Toward Flexibility

U.S. office vacancy reached ~20.2% in Q1 2026. That's not just a landlord problem — it's a signal that tenants are actively avoiding long-term lease commitments. With flex arrangements typically running 3–12 months versus traditional leases at 3–10 years, the flexibility premium is increasingly worth paying.

Market Fragmentation Is Creating Differentiation Pressure

~77% of U.S. coworking locations are run by independent or regional operators — not the major chains. That concentration of smaller players creates intense local competition. The operators who break out aren't necessarily bigger; they're more specific — whether through niche formats, ownership-based models, or hybrid-use spaces that traditional flex providers can't or won't offer.

How These Trends Are Impacting the Shared Office Industry

Operational Impact

Space design is shifting. Private office occupancy globally reached ~71.3% in mid-2025 and is rising, while open-desk areas remain stable but generate lower revenue per square foot. Operators are reconfiguring floor plans — fewer open desks, more enclosed offices and meeting rooms — to improve RevPAD (revenue per available desk), a measure of how much income each desk slot generates.

Business Impact

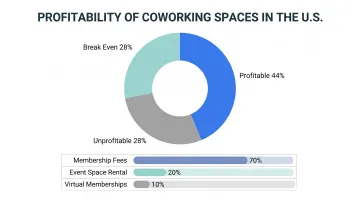

Profitability in the shared office sector is improving but uneven. Deskmag's 2025 survey found clear winners and losers:

- 54% of coworking businesses reported profits over the prior 12 months

- 18% reported losses

- Operators who diversify beyond desk memberships — adding virtual offices, event rentals, and business services — consistently outperform those who don't

Workforce and User Impact

The traditional flex space user — a Millennial freelancer in a major metro — now shares the building with corporate teams, trade businesses, and creative professionals. In response, operators are shifting amenity packages toward private phone booths, on-demand conference rooms, and specialized storage — features that serve a wider range of use cases than the open-plan perks that defined coworking a decade ago.

Future Signals for Shared Office Space in 2026 and Beyond

A few developments worth watching closely over the next 12–36 months:

- Penetration growth — coworking's share of U.S. office inventory moved from ~2.0% to ~2.2% in a single year. Markets already at 3%+ penetration show this ceiling can be pushed substantially higher

- AI personalization — matching members with events, collaborators, and resources based on behavioral data; this is the next layer after pricing automation

- Smart building integration — automated access, IoT-based energy management, and predictive maintenance are projected to deliver 15–30% energy savings in flex facilities that deploy them

- Zoning reform — municipalities are slowly updating mixed-use and light industrial classifications to accommodate hybrid-use formats; this will open new development sites in markets currently constrained by zoning

- Ownership model adoption — secondary markets in Montana, North Carolina, Colorado, and Florida are well-positioned to capture small business demand from businesses exiting expensive metros — particularly those open to buy-vs-lease Professional Work Suite formats that build equity instead of accumulating rent

Operators who track these signals now — before they're priced into the market — gain a real edge in site selection, lease negotiation, and ownership-format decisions.

Conclusion

The shared office space market in 2026 has shifted in ways that aren't temporary. Secondary markets are outpacing gateway cities, and corporate teams are committing to flex as a long-term strategy — not a stopgap. Beneath those headline trends, three quieter shifts are reshaping the landscape:

- AI-driven pricing and operations are separating efficient operators from those still running on gut instinct

- Flex industrial formats are capturing demand that traditional coworking was never designed to serve

- Ownership-based models are giving small businesses a real exit from indefinite monthly rent

Businesses and investors who act on these shifts now — picking the right market, the right format, and the right ownership model — will enter the back half of this decade with stronger margins and fewer surprises than those who wait.

Frequently Asked Questions

What does flexible office space mean?

Flexible office space refers to workspace arrangements without long-term lease commitments, typically offered month-to-month or on short-term plans. It includes coworking spaces, shared offices, hot desks, and private suites that can be scaled up or down as business needs change.

What is flex space zoning?

Flex space zoning is a land-use classification that allows a building to be used for a mix of purposes such as light industrial, office, retail, or storage, without requiring separate permits for each use type. Zoning reform in this area is expanding where hybrid-use developments can be built.

How big is the shared office space market in 2026?

The U.S. coworking and shared office market reached over 9,100 locations and 163.9 million square feet in Q1 2026. Globally, the market is valued at approximately $22 billion and is projected to grow significantly through the early 2030s.

What is the difference between shared office space and coworking?

Coworking emphasizes open, community-driven environments with built-in networking. Shared office space is a broader term covering more private setups where multiple companies share infrastructure and costs, prioritizing operational control over community programming.

Who uses shared office spaces?

Shared office spaces serve freelancers, startups, remote workers, and established corporate teams, with IT, finance, and professional services leading adoption. Hybrid-use formats are also drawing in trade businesses, creative professionals, and small operators with light-industrial or storage needs.

Is shared office space a good investment?

For operators in high-demand markets, profitability depends on location, product mix, and occupancy rates. For users, ownership-based models like those offered by Personal Warehouse let small businesses build equity rather than paying rent indefinitely.